The Magnificent Seven group, which was crafted by Mad Cash host Jim Cramer, is famend for its spectacular progress potential and its capability to roll with the financial punches. With shares of Tesla (NASDAQ:TSLA) now on the skin trying in (Cramer eliminated it from the Magnificent Seven) following its brutal quarterly flop, questions linger as to which different progress firms are extra deserving of a spot within the group.

Subsequently, on this piece, we’ll test in with TipRanks’ Comparability Device to stack up two candidates that I consider are deserving of consideration now that Tesla is now not magnificent sufficient to remain within the Magnificent Seven.

Netflix (NASDAQ:NFLX)

Bear in mind the times when the FAANG (additionally a time period and cohort created by Jim Cramer) group was dominating the monetary headlines, powering broader markets larger? In the event you’re a brand new investor who jumped into the market waters inside the previous two years, you’re most likely extra acquainted with the Magnificent Seven group. Both method, I do suppose the “N” — Netflix — within the unique FAANG is beginning to show its potential as soon as once more, and this has me extremely bullish about its future.

The inventory took an enormous beating again in late 2021 and early 2022, crashing by round 75% from peak to trough. The implosion brought about Netflix inventory to be scratched out of the dialog, in the end marking the start of the tip of FAANG and the start of the Magnificent Seven group.

Right now, Netflix is making an epic comeback, proving its doubters mistaken, with a handful of spectacular quarters which have helped gas a greater than 220% acquire off its 2022 lows. Certainly, competitors within the streaming area was getting intense, and because the pandemic lockdown winners reversed course in violent vogue, it was pure to suppose that Netflix was on its method out of the dialog.

After the newest spectacular quantity, although, Netflix has confirmed to us all that it’s nonetheless magnificent and that the 2021-22 crash was a blunder made by Mr. Market. The unique streaming kingpin stays king, with its spectacular content material that’s saved customers coming again, even following substantial value hikes. Moreover, the ad-based tier and gaming growth have made the agency extra of a progress inventory once more.

Solely time will inform if Netflix is headed for brand new heights because it continues including to its power within the new yr. Unbelievably, shares are down round 18% from their peak in 2021. With co-founder Reed Hastings slashing his stake by $1.1 billion, positive factors can be tougher to return by within the new yr. The inventory’s already endured fairly a little bit of a number of growth in current quarters. A lot in order that some analysts have been downgrading it because of valuation considerations.

At 46.8 occasions trailing price-to-earnings (P/E), the inventory is pricier than its historic common and that of its peer group. Whereas Netflix inventory deserves a premium, I consider the corporate might want to hold releasing high-quality content material and expertise extra success with its gaming push if it’s to maintain progress on the degree that warrants inclusion into the “Magnificent Seven.”

Can or not it’s completed? I feel it might probably. Administration has actually executed, and the inventory displays an enormous rebound in investor confidence.

What Is the Value Goal for NFLX Inventory?

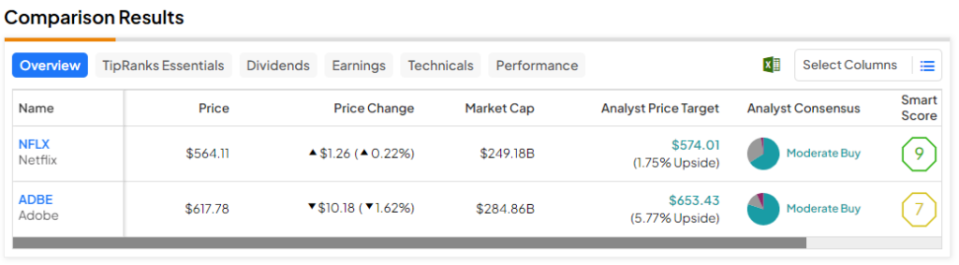

Netflix inventory is a Average Purchase, in keeping with analysts, with 27 Buys, 13 Holds, and one Promote assigned prior to now three months. The common NFLX inventory value goal of $574.01 implies 1.8% upside potential.

Adobe (NASDAQ:ADBE)

Adobe inventory is one other tech titan that’s been scorching sizzling in 2023, blasting off almost 70% prior to now yr. Generative synthetic intelligence (AI) is a big motive why Adobe inventory has been in a position to flip the tide so quick. With spectacular AI applied sciences (suppose Firefly and Sensei) ingrained into the corporate’s already spectacular artistic suite, the agency might have the technique of charging its customers much more.

If it’s including extra worth, customers ought to be greater than prepared to pay the upper value. As Adobe continues embracing the AI age, I can’t assist however keep bullish on the inventory.

In reality, I view AI because the catalyst that might propel ADBE inventory proper again to all-time highs. Lately, BakerAvenue’s King Lip said that the corporate’s AI enterprise is “extraordinarily compelling.” With such a sizeable and constant put in person base, upselling AI choices is more likely to be no subject for the agency.

It’s not nearly placing profound AI energy into artistic palms that has me most intrigued. Given the horrific headlines surrounding AI-generated deep fakes of Taylor Swift that went viral, I consider extra consideration should be positioned on AI guardrails to make sure the accountable use of AI merchandise.

In that regard, I consider Adobe is a agency that may put the suitable guardrails in place to stop (or decrease) misuse of AI instruments. As the corporate strikes on from its deserted Figma acquisition, search for the agency to change into as a lot of an AI innovator as it’s a main participant in AI security and ethics.

All issues thought of, Adobe inventory stands out as an impressive tech agency worthy of extra investor (and Cramer) reward.

What Is the Value Goal for ADBE Inventory?

Adobe inventory is a Average Purchase, in keeping with analysts, with 24 Buys, 4 Holds, and two Sells assigned prior to now three months. The common ADBE inventory value goal of $653.43 implies 5.8% upside potential.

The Takeaway

Undoubtedly, there are a slew of high-growth firms which might be doing extremely nicely, with drivers that might assist hold progress elevated for a while. That alone doesn’t assure a spot with the now six magnificent firms (the so-called Tremendous Six, if you’ll).

Nevertheless, I do suppose Netflix and Adobe are firms worthy of essentially the most unique and enviable high-growth cohort on the market. Between the 2, analysts anticipate extra upside from Adobe (5.8%) for the yr forward.