The market has rallied impressively over the previous a number of months, with the S&P 500 index reaching all-time highs that affirm a brand new bull market is underway in shares. With this latest rally, some inventory valuations could also be stretched, making it more durable to seek out offers. Excellent news for you: There are nonetheless loads of offers available out there at present.

Financial institution shares have been sluggish to get well amid the excessive rate of interest atmosphere, which has been a headwind to companies. Nonetheless, there are at the very least three financial institution shares that also commerce at extremely low cost valuations and might be poised to take off.

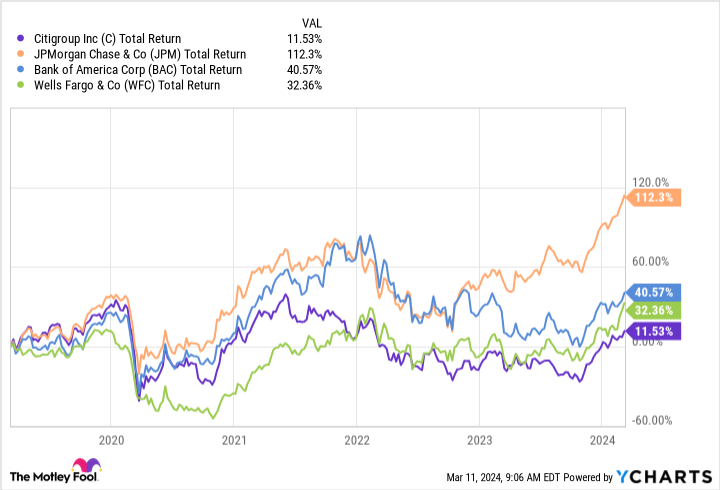

1. Citigroup

Citigroup (NYSE: C) is likely one of the largest banks within the U.S. however has struggled lately as its wide-ranging worldwide enterprise endeavors has unfold it too skinny. Not solely that, however a couple of years in the past, the financial institution was fined $400 million for deficiencies in inner controls, danger administration, and knowledge governance. Because of this, Citigroup’s efficiency struggled in contrast with that of its banking friends.

Due to its latest historical past of underperformance, Citigroup trades at a dust low cost 33% low cost to its tangible ebook worth. As compared, Financial institution of America and Wells Fargo commerce at a 44% and 54% premium to ebook worth, respectively.

Citigroup’s low cost valuation is one side that makes it interesting. Nonetheless, the steering of CEO Jane Fraser, if applied, may give Citigroup a better valuation. Fraser took over as CEO in 2021 and laid out plans to get rid of much less worthwhile operations whereas leaning into these that can increase its effectivity. As a part of this transfer, it introduced it might wind down 13 international client franchises, scale back its workforce, consolidate operations, and streamline its enterprise.

Some analysts are fairly optimistic about its technique. For instance, Wells Fargo analyst Mike Mayo believes Citi’s inventory value may attain $100 over the following three years. Whereas Citigroup has its work minimize out for it, its low cost valuation gives some margin of security and makes it appear to be a very good worth inventory to purchase at present.

2. Goldman Sachs

Rising rates of interest have dampened funding banking exercise over the previous a number of years, impacting Goldman Sachs (NYSE: GS), one of many largest funding banks on this planet.

In 2022, rising rates of interest created an air of uncertainty round markets, together with these for preliminary public choices (IPOs) and mergers and acquisitions, each bread-and-butter companies for funding bankers. In accordance with the consulting agency PwC, the IPO markets over the past two years have been a number of the lowest-volume years within the U.S. In whole, there have been 175 IPOs up to now two years, properly beneath 2021, which noticed a whopping 951 IPOs.

Goldman Sachs’ funding banking income plummeted 56% over two years ending in 2023. It has additionally made different strikes to consolidate its operations, like winding down its client enterprise, which has been struggling for the previous a number of years. The troublesome atmosphere has made it robust to be optimistic about Goldman Sachs. As we speak, the funding financial institution trades at 16.8 occasions earnings and simply 9.9 occasions one-year ahead earnings.

Nonetheless, IPO markets are exhibiting indicators of life, with Reddit, Stripe, and Klarna being a number of the most anticipated IPOs that would occur later within the yr. In the event that they launch efficiently, it might be a very good signal that danger urge for food is again. If that is the case, Goldman Sachs appears to be like like a superb cut price inventory to choose up at present earlier than we see an additional pickup in exercise.

3. Lending Membership

Lending Membership (NYSE: LC) is a consumer-focused lender that helps customers refinance their debt and roll it up into private loans. With bank card debt topping $1.13 trillion, customers have racked up debt at a time when bank card rates of interest are close to an all-time excessive.

This rising client debt may create an enormous alternative for Lending Membership. The corporate began as a peer-to-peer lending platform in 2006 however has reworked right into a client lender and a financial institution following its acquisition of Radius Bancorp in 2021. Because of this, it holds about 15% to 25% of its highest-quality loans on its books, which might generate internet curiosity earnings along with the income it earns for originating and promoting its remaining loans to the market.

LendingClub CEO Scott Sanborn advised traders, “We have been getting ready our private loans franchise to fulfill the historic refinance alternative forward.” To take action, Lending Membership is creating merchandise that permit members to comb bank card balances into fee plans. In different phrases, prospects can “high up” an current private mortgage, making it straightforward to handle their debt steadiness.

Shoppers could consolidate their loans, particularly if rates of interest fall, benefiting LendingClub’s core enterprise. If that is the case, now might be a superb time to scoop up shares, that are cheaply priced at an 18% low cost to tangible ebook worth and 11 occasions ahead earnings, forward of this historic refinancing alternative.

Must you make investments $1,000 in Citigroup proper now?

Before you purchase inventory in Citigroup, think about this:

The Motley Idiot Inventory Advisor analyst staff simply recognized what they imagine are the 10 greatest shares for traders to purchase now… and Citigroup wasn’t considered one of them. The ten shares that made the minimize may produce monster returns within the coming years.

Inventory Advisor gives traders with an easy-to-follow blueprint for fulfillment, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than tripled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of March 11, 2024

Financial institution of America is an promoting associate of The Ascent, a Motley Idiot firm. Wells Fargo is an promoting associate of The Ascent, a Motley Idiot firm. JPMorgan Chase is an promoting associate of The Ascent, a Motley Idiot firm. Citigroup is an promoting associate of The Ascent, a Motley Idiot firm. Courtney Carlsen has positions in LendingClub. The Motley Idiot has positions in and recommends Financial institution of America, Goldman Sachs Group, and JPMorgan Chase. The Motley Idiot has a disclosure coverage.

3 Extremely Low cost Financial institution Shares to Purchase Now was initially printed by The Motley Idiot