The Nasdaq-100 Expertise Sector index has gained 7% throughout the first two months of 2024, and it will not be stunning to see it soar larger because the 12 months progresses, due to the proliferation of synthetic intelligence (AI).

AI shares have performed a giant position in boosting the Nasdaq-100 up to now 12 months, sending the index up almost 54% as its elements, akin to Nvidia (NASDAQ: NVDA) and Meta Platforms (NASDAQ: META), have delivered gorgeous positive aspects of 233% and 181%, respectively. Historical past means that the Nasdaq-100 tends to leap 24% on common following a 12 months wherein it achieved positive aspects of 40% or extra.

So, it will not be stunning to see the Nasdaq soar larger in 2024, particularly contemplating the newest outcomes from Nvidia and Meta Platforms. Let us take a look at the explanation why these two tech giants are all set to spice up the Nasdaq and in addition test why now shall be an excellent time to purchase them.

1. Nvidia

Nvidia’s inventory market rally bought a pleasant increase after the corporate launched fiscal 2024 fourth-quarter outcomes (for the three months ended Jan. 28, 2024) on Feb. 21. The chipmaker cruised previous consensus estimates with document quarterly income of $22.1 billion, a soar of 265% from the year-ago interval.

The corporate was initially anticipating its fiscal This fall income to land at $20 billion. Nevertheless, its efforts to extend the provision of its flagship H100 AI graphics processing unit (GPU) to fulfill the sturdy demand from clients helped it ship stronger-than-anticipated development.

That is not stunning as Nvidia’s foundry associate, Taiwan Semiconductor Manufacturing, popularly referred to as TSMC, has been aggressively growing its superior packaging capability in order that it could churn out a larger variety of AI chips. Provide chain sources point out that TSMC’s chip-on-wafer-on-substrate (CoWoS) manufacturing capability, which is used for making AI chips, is ready to develop to 33,000 to 35,000 wafers a month by the fourth quarter of 2024. That will be greater than double TSMC’s estimated month-to-month CoWoS capability of 15,000 wafers in December 2023.

Not surprisingly, Nvidia administration identified on the newest earnings convention name that the provision of its AI graphics playing cards is enhancing. However what’s attention-grabbing to notice right here is that Nvidia expects the demand for its GPUs to outpace provide regardless of the efforts it’s endeavor to provide extra chips. In response to CFO Colette Kress, the corporate expects its “next-generation merchandise to be provide constrained as demand far exceeds provide.”

Nvidia will begin ramping up the shipments of its next-generation H200 AI GPU within the second quarter. The corporate is claiming that this chip “almost doubles the inference efficiency of H100,” which does not appear stunning as it’s anticipated to be manufactured utilizing a extra superior 3-nanometer (nm) chipmaking course of as in comparison with the H100’s 5nm course of. Furthermore, Nvidia is packing the H200 with extra reminiscence bandwidth and capability.

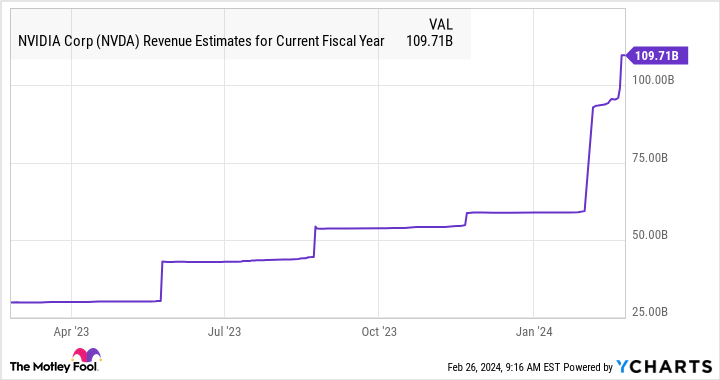

Because of this, Nvidia appears to be in a stable place to keep up its spectacular share of the $67 billion AI chip market in 2024. Gartner estimates that $53 billion value of AI chips had been bought final 12 months, and Nvidia’s knowledge middle income of $47.5 billion signifies that it managed 90% of this market final 12 months. An analogous share this 12 months can assist Nvidia maintain its momentum, which explains why its fiscal 2025 income is predicted to extend 83% to $110 billion.

The market might reward such spectacular development with extra upside. With shares of Nvidia buying and selling at 33 occasions ahead earnings, which is decrease than the Nasdaq-100’s earnings a number of of 34, traders would do effectively to purchase this AI inventory straight away since its bull run appears right here to remain.

2. Meta Platforms

Identical to Nvidia, Meta Platforms is buying and selling at a sexy 24 occasions ahead earnings. Shopping for Meta inventory at this valuation seems like a no brainer, contemplating that its backside line is predicted to leap a formidable 34% in 2024 to $19.91 per share. Even higher, analysts are anticipating Meta’s earnings to extend at an annual fee of 26% for the following 5 years, a giant enchancment over the 11% annual earnings development it has clocked up to now 5 years.

Assuming Meta can obtain this tempo of bottom-line development, its earnings might enhance to $47.22 per share after 5 years, utilizing its 2023 earnings of $14.87 per share as the bottom. If we multiply the projected earnings after 5 years with Meta’s five-year common ahead earnings a number of of 21, its share worth might enhance to $991. That will be a stable soar of 105% from present ranges.

AI is a key purpose why Meta ought to be capable of ship the stable earnings development that analysts expect from it. The corporate has been integrating generative AI into its promoting instruments to assist advertisers enhance concentrating on and generate stronger returns on the promoting {dollars} they spend. From serving to advertisers create a number of backgrounds for his or her advert campaigns primarily based on product photos to producing advert texts, Meta believes that its Adverts Supervisor platform can “unlock a brand new period of creativity that maximizes the productiveness, personalization and efficiency for all advertisers.”

Meta factors out that utilizing generative AI in promoting has the potential to assist advertisers save 5 or extra hours each week whereas additionally boosting returns on advert spending by 32%. Because of this, it will not be stunning to see Meta cornering an even bigger share of the digital advert market, just like what it did final 12 months. The corporate’s 2023 income elevated by 16% to $134.9 billion, outpacing the ten.7% enhance in digital advert spending.

This 12 months, analysts are forecasting a 17.3% enhance in Meta’s income to $158.2 billion, suggesting that it’s on monitor to outpace the 13.2% projected development in digital advert spending, as per eMarketer. The digital advert market is predicted to leap to an estimated $1.5 trillion in 2030 as in comparison with $531 billion in 2022. So, Meta’s give attention to utilizing AI to enhance its affect on this market means that it’s setting itself up for long-term development, which is why traders ought to think about shopping for Meta inventory earlier than it soars additional.

Do you have to make investments $1,000 in Nvidia proper now?

Before you purchase inventory in Nvidia, think about this:

The Motley Idiot Inventory Advisor analyst crew simply recognized what they imagine are the 10 greatest shares for traders to purchase now… and Nvidia wasn’t considered one of them. The ten shares that made the lower might produce monster returns within the coming years.

Inventory Advisor offers traders with an easy-to-follow blueprint for fulfillment, together with steerage on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than tripled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of February 26, 2024

Randi Zuckerberg, a former director of market improvement and spokeswoman for Fb and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Idiot’s board of administrators. Harsh Chauhan has no place in any of the shares talked about. The Motley Idiot has positions in and recommends Meta Platforms, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Idiot recommends Gartner. The Motley Idiot has a disclosure coverage.

2 Synthetic Intelligence (AI) Shares to Purchase Hand Over Fist Earlier than the Nasdaq Soars Greater in 2024 was initially revealed by The Motley Idiot