If you’re wanting on the oil sector, you will need to ensure you contemplate {industry} giants which have confirmed they will face up to the inherent volatility of power costs.

Two of the most effective choices are ExxonMobil (NYSE: XOM) and Chevron (NYSE: CVX). However one other selection additionally to think about is TotalEnergies (NYSE: TTE), which has taken a drastically totally different method to scrub power funding.

All three may be purchased for lower than $200 a share and traders ought to be capable to comfortably maintain them for a really, very very long time.

Exxon is the {industry} big

With a market cap of round $380 billion, Exxon is the oil {industry}’s 800-pound gorilla. That alone is not sufficient to make the inventory a purchase, however it has the heft to compete with any firm within the house. Add in a diversified portfolio, which spans drilling (upstream), transportation (midstream), and refining and chemical substances (downstream), and it’s fairly near a one-stop store within the power sector.

The worth of utilizing this built-in mannequin is that some areas (downstream) can carry out effectively when oil costs are low, successfully serving to to offset the ache from areas (upstream) which can be more likely to be performing poorly. Though this solely helps to melt the ache of oil busts, it additionally helps to make Exxon a extra secure firm over time.

That’s highlighted by the 41 years of annual dividend will increase this firm has achieved regardless of working in a extremely cyclical {industry}. The opposite key to the corporate’s dividend resilience is its sturdy stability sheet, with a debt-to-equity ratio of simply 0.2 or so. That is the second-best amongst its closest friends.

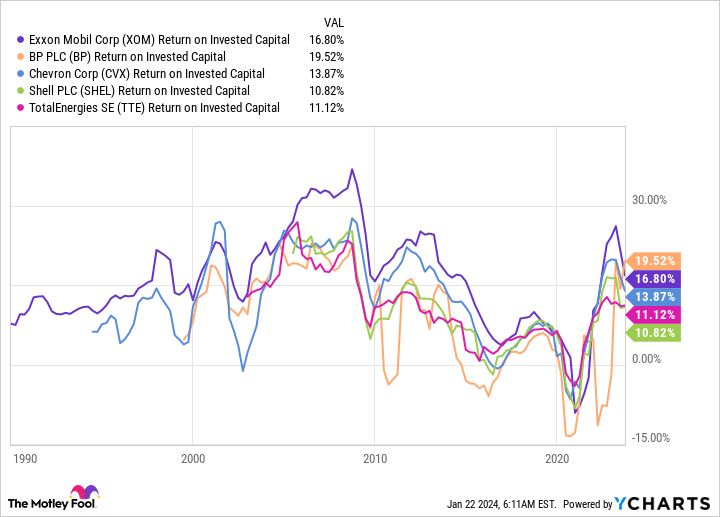

However the actual purpose to love Exxon might be its lengthy historical past of being at or close to the highest of the peer group for return on invested capital, a measure of how effectively it’s utilizing shareholder cash. That is the kind of firm you need to personal.

Chevron has a better yield and stronger basis

Chevron and Exxon are very related corporations. Chevron is a bit smaller, with a market cap of “simply” $260 billion or so. And whereas Chevron’s dividend file is not fairly pretty much as good, it’s onerous to complain an excessive amount of about an organization that is elevated its dividend yearly for 36 years. If you’re Exxon, you ought to be Chevron, too.

That stated, Chevron shines brighter than Exxon in two vital methods. First, Chevron’s 4.2% dividend yield is bigger than Exxon’s 3.9%. And second, Chevron’s debt-to-equity ratio is decrease at 0.12. That is extra revenue from a financially stronger firm.

That is notable, provided that each Chevron and Exxon lean on their stability sheets throughout unhealthy oil markets to allow them to proceed to assist their companies and dividends. For extra conservative dividend traders, Chevron may very well be the higher long-term funding selection.

TotalEnergies is making ready immediately for a unique tomorrow

There’s one potential downside to investing in Exxon or Chevron, as each are persevering with to focus closely on the oil enterprise. For those who assume that the clear power transition is more likely to upend the oil sector, you will most likely desire an organization that is addressing the problem now, like France-based TotalEnergies.

To be truthful, BP and Shell have additionally made a extra dramatic shift than Exxon or Chevron within the clear power course. However BP and Shell minimize their dividends after they introduced these plans. TotalEnergies made the identical pivot and maintained its dividend.

This is not to recommend that TotalEnergies is a clear power inventory — that is simply not the case. Its built-in energy enterprise solely makes up round 7.5% of its enterprise phase working revenue. However it’s persevering with to spend money on the enterprise and refine its publicity to grease, refocusing round solely its greatest alternatives.

Basically, this built-in power big is providing traders a hedged guess within the oil house. And it has an industry-leading dividend yield of 5%.

All for lower than a grand

Exxon, Chevron, and TotalEnergies are all oil corporations you possibly can comfortably personal for years to come back. That stated, there are refined nuances which can be essential amongst this trio of built-in power corporations. Dig in and you will doubtless discover one that’s of curiosity and that matches your particular funding wants. One of the best half is you will get began with as little as $200.

Must you make investments $1,000 in Chevron proper now?

Before you purchase inventory in Chevron, contemplate this:

The Motley Idiot Inventory Advisor analyst group simply recognized what they consider are the 10 greatest shares for traders to purchase now… and Chevron wasn’t considered one of them. The ten shares that made the minimize may produce monster returns within the coming years.

Inventory Advisor offers traders with an easy-to-follow blueprint for achievement, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than tripled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of January 22, 2024

Reuben Gregg Brewer has positions in TotalEnergies. The Motley Idiot has positions in and recommends BP. The Motley Idiot recommends Chevron. The Motley Idiot has a disclosure coverage.

Obtained $200? 3 Oil Shares to Purchase and Maintain Perpetually was initially revealed by The Motley Idiot