One of many oddest and most mysterious relationships that emerged out of the collapse of FTX final yr was Alameda Analysis’s uncommon relationship with Farmington State Financial institution, one of many smallest, rural banks in the USA that got here underneath the management of Jean Chalopin in 2020. Chalopin is greatest often called the chairman of Deltec, one of many major banks for Alameda Analysis – FTX’s buying and selling arm that performed a central position in its collapse — and nonetheless one of many major banks for the most important fiat-backed stablecoin, Tether (USDT). Chalopin had acquired management over Farmington through FBH Corp., the place Chalopin was listed as government officer. Apparently, Noah Perlman, a former DOJ and DEA official who’s now Chief Compliance Officer at Binance and the son of Jeffrey Epstein affiliate and musician Itzhak Perlman, was additionally listed as a director of FBH Corp and has by no means publicly defined his reference to this Chalopin-controlled entity.

As Limitless Hangout reported final December, quickly after its acquisition by Chalopin’s FBH Corp., Farmington “pivoted to take care of cryptocurrency and worldwide funds” after a long time upon a long time of serving as a single department group financial institution in rural Washington. Quickly after its pivot into the crypto house, Farmington struggled to maneuver cash and sought approval to change into a part of the Federal Reserve system. It additionally modified its identify from Farmington State Financial institution to Moonstone Financial institution. The approval of Farmington by the Federal Reserve has been deemed extremely uncommon and as having “glossed over Moonstone’s for-profit international pursuits.” Late final December, Eric Kollig, spokesman for the Federal Reserve, instructed reporters that he couldn’t remark “concerning the course of that federal regulators undertook to approve Chalopin’s buy of the constitution of Farmington State Financial institution in 2020.”

Simply days after Farmington formally modified its identify to Moonstone in early March 2022, FTX-affiliated Alameda Analysis poured $11.5 million into the financial institution, which was – on the time – greater than twice its total web price. Moonstone’s Chief Digital Officer, Jean Chalopin’s son Janvier, later acknowledged that the funding from Alameda Analysis had been “seed funding … to execute our new plan of being a tech-focused financial institution.”

Upon Alameda’s taking a stake within the financial institution, Jean Chalopin acknowledged that this transfer “signifies the popularity, by one of many world’s most modern monetary leaders, of the worth of what we’re aiming to attain. This marks a brand new step into constructing the way forward for banking.” Retailers like Protos have famous how uncommon it’s {that a} Bahamas-based firm like FTX was “in a position to buy a stake in a federally authorized financial institution” with out attracting the eye of regulators.Washington State regulators have acknowledged that they had been “conscious” of Alameda’s funding in Farmington/Moonstone and defended their choice to not intervene or take additional regulatory motion.

Notably, the inflow of recent cash into the transformed Farmington was not unique to FTX/Alameda. A New York Occasions article on the matter famous that Farmington/Moonstone’s deposits – which had hovered round $10 million for a lot of a long time – shortly surged to $84 million, with $71 million coming from solely 4 new accounts throughout this identical comparatively quick interval in 2022.

As Limitless Hangout beforehand famous, the identical day the Alameda funding was introduced, Moonstone put in Ronald Oliveira as CEO. Oliviera had beforehand labored for the fintech firm Revolut, a “main digital various financial institution” financed by Jeffrey Epstein affiliate Nicole Junkermann. Roughly two months later, the financial institution employed Joseph Vincent as its authorized counsel. Instantly previous to becoming a member of Farmington/Moonstone, Vincent had served as the overall counsel for Washington State’s Division of Monetary Establishments and its director of authorized and regulatory affairs for 18 years.

Shortly earlier than FTX’s collapse, which put Farmington/Moonstone underneath heavy scrutiny, Farmington/Moonstone partnered with a comparatively unknown firm referred to as Fluent Finance. Fluent Finance, each then and now, has evaded scrutiny from the media apart from Limitless Hangout’s investigation into Farmington, revealed final December. Nonetheless, since FTX’s unraveling and the shuttering of Farmington/Moonstone within the months that adopted, Fluent Finance has been fairly busy, creating vital authorities partnerships within the Center East and seeking to change into a central a part of the approaching Central Financial institution Digital Forex (CBDC) paradigm for each West and East.

A possible motive behind the shortage of media curiosity in Fluent Finance and their obvious success after the FTX scandal is the truth that Fluent, from its earliest days, has been working as an obvious entrance for among the strongest business banks on the planet and constructing out “trusted” digital infrastructure for the economic system to come back. This investigation, an examination of Fluent’s previous and its present trajectory, could assist elucidate the true motives behind the efforts of Chalopin, Bankman-Fried and others to show the tiny Farmington State Financial institution into “Moonstone.”

Fluent Finance’s Deep and Early Connections to Wall Road Banks

Fluent Finance was created in 2020 and was co-founded by Bradley Allgood, Oliver Gale and Jaime Plata. Allgood started his profession with the US Military and later went on to serve in NATO’s Governmental Operations division with an obvious concentrate on NATO exercise in Afghanistan. After leaving NATO, Allgood “instantly jumped” into financial improvement, particularly the creation and enlargement of Particular Financial Zones (SEZs), particularly one partnered with the Catawba Indian Reservation in South Carolina. That SEZ, formally named the Catawba Digital Financial Zone, was co-founded by Allgood in 2019 and he nonetheless serves as its head of Business Banking.

Sitting on simply two acres of land, the zone goals to “change into the worldwide registration hub for crypto firms” in addition to to “take an enormous chunk out of Delaware’s marketplace for firm registration and even to interchange it because the gold customary.” The zone is backed by a enterprise capital agency tied to Bradley Tusk, the previous Deputy Governor of Illinois underneath disgraced former Governor Rod Blagojevich and the previous marketing campaign supervisor for billionaire Mike Bloomberg. As well as, Tusk’s firms rely Google, the Rockefeller Basis and Ripple (XRP) amongst their purchasers. Tusk’s completely different VC companies have invested in Coinbase and Circle, the issuer of the USDC stablecoin, and Uber in addition to the financial zone co-founded by Allgood.

Shortly after leaving the army, Allgood additionally labored on the early improvement of digital transformation of governments, digital identities, individuals and property registries and the tokenization of carbon credit and commodities. Later motivated by “the sheer variety of unbanked and underbanked on the planet”, Allgood hosted roundtables around the globe with central financial institution “regulators, tier one establishments, innovators, [and] expertise suppliers” and determined he might act as “an excellent connector” for the completely different actors in his rising community.

Allgood claims to have spoken to a couple “actually senior” banking executives at HSBC, Citi and Barclays and to have educated “them on new modern applied sciences for custody [and] higher digital id.” After “constructing a workforce” of those “senior bankers from tier one monetary establishments,” Allgood and his workforce “went out into the market and began servicing the [cryptocurrency] house and serving to modern firms discover houses and enormous core banking techniques and tier one monetary establishments.” Whereas working with these numerous titans of finance and guiding their views on the way forward for banking, Allgood met his co-founders of Fluent Finance: Oliver Gale and Jaime Plata.

Oliver Gale is without doubt one of the co-founders of Central Financial institution Digital Currencies (CBDCs), having pioneered the primary CBDC venture within the Japanese Caribbean and, per Allgood, Gale “went on to do them in Nigeria” and helped create the extremely controversial e-Naira. Gale notably describes himself because the inventor of CBDCs and has beforehand collaborated with the UN, MIT and the IMF. Jaime Plata, Fluent’s different co-founder, “did the core banking techniques of the Japanese Caribbean Central Financial institution in the course of the first CBDC [launch].” Except for Gale and Plata, Allgood has revealed that different high Fluent Finance executives, who should not listed on the corporate’s web site, hail from the Wall Road titan Citi – with the corporate’s CFO being “the CFO of Citi of all of Latin America” and its COO being “one of many senior, most senior, managing administrators from Citi.” He has additionally acknowledged that different essential staff of Fluent embody the previous chief innovation officer of Normal Electrical in addition to “an early board member at [the now collapsed crypto exchange] Celsius [that] helped them get to market.”

Fluent Finance was initially based with two major and interrelated merchandise: the Fluent Protocol and the US+ stablecoin. Fluent has described the Fluent Protocol as “a monetary community that seamlessly bridges conventional finance and digital belongings,” whereas US+ is a “bank-led”, US dollar-pegged stablecoin “constructed on ideas” and designed to be “forward-compatible with CBDC initiatives.” Fluent asserts that US+ resolves “the inherent flaws of web3-native stablecoins” by having US+ be operated by a community of banks partnered with Fluent Finance. Fluent has not made the identities of those banks out there to the general public.

“Once we examined stablecoins, we knew that the shortage of institutional uptake of the expertise was on account of danger,” defined Allgood. “With that in thoughts, once we approached the design of US+, we did so when it comes to de-risking. We knew we wanted to supply real-time and clear reserves monitoring.” Fluent’s reply to offering the reserve metrics wanted to faucet into the closely regulated conventional finance market emerged by way of its partnership with Chainlink, first introduced in September 2022.

Chainlink is a blockchain oracle community, which means it connects blockchains to exterior techniques. It was launched in 2017 on the Ethereum blockchain and later registered within the Cayman Islands as SmartContract Chainlink Restricted SEZC in March 2019. In December 2021, the previous Google CEO Eric Schmidt, who has unprecedented management over the Biden administration’s expertise insurance policies, joined Chainlink Labs as a strategic advisor. On the time, Schmidt commented that “it has change into clear that one in all blockchain’s biggest benefits — a scarcity of connection to the world exterior itself — can also be its greatest problem.”

Fluent’s partnership with Chainlink handled regulatory requirements by offering a dependable manner for the Fluent Protocol to entry real-time, off-chain information from exterior sources. Fluent’s objective was/is to supply proof of the scale, efficiency, and danger of its asset reserves so as to meet its stablecoin protocol liquidity necessities. Dependable affirmation and publishing of the state of those reserves was seen as essential by Allgood and others at Fluent so as to manufacture belief from each retail customers and membership banks.

Fluent is much from the one associate of Chainlink engaged on offering trusted stablecoin reserve structure. Amongst them is Paxos, the previous issuer of Binance’s BUSD and their very own PAX, and who just lately started offering infrastructure for PayPal’s PYUSD stablecoin. Paxos relied on Chainlink to supply on-chain Proof of Reserve Information Feeds for Paxos’ belongings, making certain verification that PAX tokens are 1:1 backed by US {Dollars}. This was taken a step additional with their gold-backed PAXG tokens, wherein Chainlink claimed to have the ability to present verification of off-chain, bodily gold bars held in Paxos’ custody.

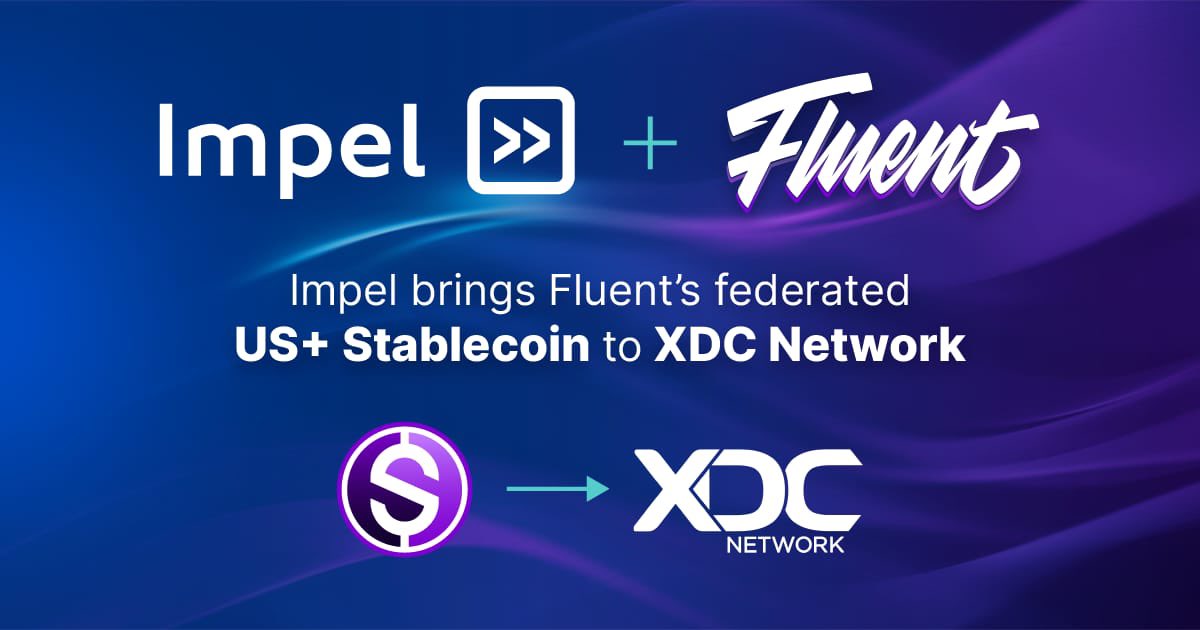

One other Chainlink associate is the XinFin Community, also called the XDC community, which makes use of Chainlink’s Value Reference Information framework to introduce value feeds for main nationwide currencies such because the Hong Kong Greenback, the Singaporean Greenback, and the United Arab Emirates Dirham. In October 2022, Fluent Finance introduced a partnership with Impel to convey its US+ stablecoin to the XDC community. Impel itself is a startup birthed out of XinFin Fintech led by CEO and founder Troy S. Wooden. The corporate boasts a workforce of advisors together with XDC Community co-founders Ritesh Kakkad and Atul Khekade, along with very long time SWIFT worker André Casterman.

In March 2021, XinFin leveraged the DASL Crypto Bridge designed by LAB577 to convey their XDC token to R3’s Corda blockchain. R3 started as a consortium of banks and isn’t solely intently linked to Fluent Finance, however, as shall be mentioned shortly, can also be a significant driver of CBDC and stablecoin improvement globally. Earlier than this XDC-Corda bridge was created, there was no liquidity or token of worth on the R3 Corda Community. This bridge opened up the chance for conventional monetary establishments, similar to people who fund R3, to work together with cryptocurrency not directly with out having to function on under-regulated public networks that would land them in scorching water with regulators. It additionally provides entry to these already using Ethereum-based tokens (i.e. ERC20 or ERC721) to the enterprise networks and monetary establishments on the Corda community.

XDC co-founder and Impel advisor Atul Khekade remarked that the each authorities regulators and business banks had settled on XDC and Corda because the means by way of which many main banks would entry blockchain applied sciences:

“Regulatory businesses and monetary establishments have chosen each Corda and the XDC Community as appropriate platforms to interact with blockchain expertise […] They didn’t simply randomly throw a dart at a board.”

Fluent Meets Moonstone

In late October 2022, Fluent Finance, now deeply ensconced within the Web3 ambitions of main business banks, introduced its partnership with Farmington/Moonstone. In a press launch on the partnership, Fluent wrote that “Moonstone shall be a custody associate in Fluent’s rising community of banks, with plans to develop right into a full-node member quickly,” which might “permit Fluent and Moonstone to attach the normal monetary system to the rising Web3 economic system.”

On the time the partnership was introduced, Fluent’s CEO Bradley Allgood acknowledged the next:

“Moonstone Financial institution is now a key participant in Fluent’s monetary ecosystem and can function an preliminary custodian associate. Fluent plans to finally convey Moonstone Financial institution on as a full-node associate, which can permit the financial institution to mint and burn US+. Collaborating with Moonstone is extremely thrilling and can assist Fluent convey a protected and safe stablecoin to market whereas permitting for immediate funds together with decrease charges. It can additionally clearly reveal the advantages that stablecoins can convey to the banking sector, companies, and on a regular basis finish customers alike.”

Notably, this was – and stays – the one Fluent Finance press launch to call a member of Fluent’s consortium that helps its “bank-led” stablecoin, US+. As well as, given Allgood’s statements on the partnership, he clearly felt that partnering with Moonstone was a essential a part of bringing US+ to market.

Nonetheless, with the collapse of FTX that November, Farmington/Moonstone got here underneath heavy scrutiny, even attracting the eye of U.S. Senators who cited Farmington/Moonstone’s relationship with FTX as motive to launch federal investigations into the relationships between banks and cryptocurrency companies. The numerous unanswered questions on Alameda’s relationship with Farmington/Moonstone, Chalopin’s involvement and potential connections to Deltec and Tether in addition to the obvious negligence of regulators brought on main reputational and belief points for Farmington/Moonstone.

Just a few months after the FTX collapse, in January 2023, Farmington introduced it might drop the Moonstone identify and return to its “unique mission as a group financial institution” and would discontinue “its pursuit of an innovation-driven enterprise mannequin to develop banking companies for industries similar to crypto belongings or hemp/hashish.” Only a few days after that announcement, federal prosecutors seized $50 million from Farmington/Moonstone, which they alleged had been deposited as “a part of FTX founder Sam Bankman-Fried’s wide-ranging scheme to defraud traders by way of his huge cryptocurrency change enterprise.” That sum, considerably greater than what Alameda Analysis had initially invested, was greater than half of the financial institution’s complete belongings primarily based on the latest FDIC filings on the time of the seizure. The $50 million seized was all underneath one account underneath the identify of “FTX Digital Markets,” per courtroom information cited by native Washington newspapers.

Then, in Could, the financial institution introduced it might be promoting its deposits and belongings to the Financial institution of Japanese Oregon. The Federal Reserve subsequently took enforcement motion in opposition to Farmington in addition to its dad or mum FBH Corp. just a few months later in August. In line with native newspapers, the Fed “issued a cease-and-desist order in opposition to the companies and directed them to take a variety of actions as Farmington closes its enterprise – together with preserving information and never buying any further brokered deposits.” The Fed asserted that Farmington had violated commitments it had made as a part of the approval course of which granted it entry to the Federal Reserve system. Nonetheless, it’s unknown which commitments had been allegedly violated, because the Fed has refused to come back clear about its extremely uncommon and irregular approval of Farmington/Moonstone, even after its enforcement actions in opposition to the financial institution. Fluent Finance issued a press release after the Fed’s announcement and referred to Farmington for the primary time as a “prior tentative” collaborator and sought to distance itself from the financial institution. Most just lately, in November, FBH Corp., Jean Chalopin’s automobile for buying after which controlling Farmington, did not file an annual report in Washington State for 2023, which means that it is going to be terminated someday inside December.

Whereas 2023 couldn’t have been worse for Moonstone/Farmington, Fluent Finance managed to efficiently reinvent itself by partnering with the federal government of the United Arab Emirates (UAE) and R3, a blockchain firm that focuses on accelerating digital currencies (significantly CBDCs) and is backed by among the greatest banks on the planet.

Constructing the Rails for CBDC settlement within the UAE

In late July, just a few weeks earlier than the Fed introduced its enforcement motion in opposition to Farmington/Moonstone, Fluent Finance introduced that they might be opening an workplace in Abu Dhabi within the United Arab Emirates, an enlargement explicitly backed by the UAE Ministry of Economic system. In line with a press launch, “As a part of their transfer into the area, Fluent Finance is getting assist from the workplace of the Ministry of Economic system, additional cementing their relationship with regulators and leaders within the area to unveil modern options for cross-border funds.” The UAE authorities was explicitly backing Fluent Finance in order that the corporate might “advance the UAE’s commerce finance and cross-border funds panorama.”

Fluent’s new UAE entity, referred to as Fluent Financial Bridge, focuses on deposit tokens, i.e. business bank-issued tokens backed by deposits, with the specific intention of connecting deposit token and CBDC techniques inside the UAE and, finally, past. As beforehand talked about, Fluent is partnered with the corporate R3, which is presently underneath contract with the UAE’s Central Financial institution to construct out the nation’s CBDC system. Fluent Financial Bridge makes use of R3’s Corda DLT (distributed ledger expertise) so as to “convey CBDC-compatible deposit token infrastructure for borderless funds.”

Just a few months later, in October, Fluent Finance – described in reviews from this era as a “US-based developer of a cryptocurrency-based cost platform” – joined an UAE authorities program referred to as NextGenFDI, which goals to supply a litany of incentives to international web3-focused firms to relocate to the nation. Experiences praising Fluent’s participation in this system famous that Fluent’s focus had moved to “mak[ing] cross-border commerce simpler” and that the corporate’s UAE-based Fluent Financial Bridge can be “utilized by importers and exporters to settle transactions by way of bank-issued cryptocurrencies, often called stablecoins or deposit tokens.” “I’m optimistic concerning the potentialities of the Fluent Financial Bridge, and the potential for digital currencies to enhance the effectivity and accessibility of worldwide provide chains,” UAE Minister of State for International Commerce Dr. Thani Al Zeyoudi was quoted as saying.

:quality(70)/cloudfront-eu-central-1.images.arcpublishing.com/thenational/CVJ5VDESGRAQBP2LQATMU2F4AQ.jpg)

Fluent’s collaboration with the UAE authorities was notably designed to align “with the [UAE’s] Ministry of Economic system’s TradeTech initiative, which, with the participation of the World Financial Discussion board, goals to advertise the usage of superior expertise instruments in world provide chains, in addition to the nation’s complete financial partnership settlement programme, which goals to attain frictionless commerce between the UAE and different economies.”

Articles on the event additionally acknowledged that “by working with banks and regulators in Abu Dhabi, Fluent goals to spice up the transparency of cryptocurrency with the safety and regulatory construction of the normal banking system.” Claims had been made that Fluent has been piloting this program in Kenya, however Fluent’s web site makes no point out of any such program and no details about any such pilot is obtainable on-line on the time this text was revealed. This implies that Fluent’s pilot in Kenya is working underneath a special identify with no overt ties to the corporate being publicized.

Just a few days later, Emirati information reported that Fluent Finance can be partnering with the UAE’s Ministry of Economic system to develop “deposit token-based tech” and “stablecoin applied sciences.” The corporate acknowledged that by “collaborating with banks and regulators[,] its platform gives the immediacy and transparency of cryptocurrency with the safety and regulatory construction of the normal banking system.” Allgood framed a lot of the collaboration as a key a part of the UAE’s effort to “modernize” multilateral commerce. He acknowledged that “The UAE has positioned itself as a world chief for digital belongings by way of their particular financial zone initiatives, regulation foresight, and world commerce enlargement with strategic MoUs [memorandums of understanding],” particularly MoUs with India and China, key members of the BRICS bloc. Since these reviews, much more MoUs have been signed between the UAE and BRICS nations. For example, earlier this month, China’s central financial institution signed a $400 million “cooperation memorandum” with the UAE’s central financial institution that’s particularly centered on the interchange of the nations’ respective CBDCs. As beforehand famous, the UAE’s coming CBDC, the digital dirham, is being developed by R3, which is intently tied to Fluent Finance.

A report in Gulf Enterprise on Fluent’s collaborations with the UAE famous that, with respect to the MoUS, “the agreements account for greater than $100bn in bilateral commerce, with a concentrate on strengthening the usage of new applied sciences and settlement with digital foreign money. Deposit tokens issued by business banks are poised to supply a borderless lacking hyperlink to speed up commerce settlement to central financial institution digital foreign money.” In different phrases, plainly Fluent is positioning itself as an accelerator for CBDCs through deposit tokens, associated infrastructure and its “low counterparty danger stablecoin” US+.

R3 – Accelerating Monetary Surveillance

Additional proof of Fluent’s intentions to speed up a CBDC-deposit token paradigm might be present in Fluent Finance’s cozy relationship with R3, a self-described “chief within the digitization of monetary companies” that’s answerable for the Corda DLT platform. As beforehand talked about, R3’s backers embody among the greatest names in finance, amongst them a number of of the huge business banks who had an early position within the creation of Fluent Finance.

Fluent’s reference to R3 was current early on, together with earlier than its ill-fated try and associate with Farmington/Moonstone. For example, Fluent’s early partnership with XDC in October 2022 was influenced by the truth that XDC was additionally “closely associated to R3” in addition to XDC’s concentrate on “commerce finance” in keeping with Allgood. Notably, XDC can also be very lively within the UAE and was described by Emirati media as a “driving drive” behind the nation’s ambition to change into “the successor to Silicon Valley” in articles revealed roughly a month earlier than Fluent introduced its partnership with the UAE’s Ministry of Economic system.

As well as, Fluent’s head of engineering Will Hester, who joined the corporate in April 2022, beforehand labored as R3’s tech lead and beforehand as a R3 software program engineer. Different Fluent staff, similar to software program engineer John Buckle, had additionally beforehand labored for R3. As well as, Fluent Finance’s US+ makes use of a non-public Corda community (Corda being a R3 product) to tokenize US+’s fiat foreign money (i.e. US $) reserves. Experiences on Fluent’s enlargement into the UAE word that the corporate selected to make use of Corda so as to “introduce CBDC-compatible deposit token infrastructure for borderless funds.”

Whereas Fluent has been comparatively quiet about its business banking companions, what Allgood has revealed is an obvious affiliation between the early days of the corporate with HSBC, Citi and Barclays, suggesting that these banks might be among the many members of its banking consortium backing its US+ stablecoin. R3, which notably started as a consortium of business banks, is backed by main banks together with HSBC, Citi and Barclays in addition to different high names in finance together with BNY Mellon (which now holds the majority of the reserves for the USDC dollar-pegged stablecoin after the banking disaster earlier this yr), Deutsche Financial institution and Wells Fargo. R3’s relationship with Wells Fargo is especially notable as the corporate’s Corda platform is taking part in a essential position in Wells Fargo’s pilot of a dollar-pegged stablecoin that shall be used “initially for inner settlement throughout the corporate’s enterprise.” The Wells Fargo dollar-pegged stablecoin on Corda is being pitched for primarily the identical use instances as Fluent’s US+.

Although R3 has appreciable ties to a coming digital greenback, by way of Wells Fargo, Fluent Finance and others, they’re additionally a key participant in a variety of CBDC tasks globally. As beforehand talked about, in April of this yr, the UAE introduced that it had chosen R3 to start implementing its CBDC technique. The corporate, which describes itself as having been “on the forefront of CBDC innovation since 2016,” can also be concerned with CBDC improvement in France, Kazakhstan, South Africa, Australia, Malaysia, Switzerland, Singapore, and Sweden and is partnered immediately with the central banks of these nations. R3 was additionally concerned in Italy’s Undertaking Leonidas, a wholesale CBDC trial between Italy’s central financial institution and the Italian Banking Affiliation. R3 was even named 2023’s CBDC associate of the yr by the publication Central Banking.

Nonetheless, R3 is targeted on way more than CBDCs, as evidenced by their Digital Forex Accelerator (DCA), which presents “an end-to-end resolution that allows central banks, business banks, and financial authorities to points, handle, transact, and redeem CBDCs and privately-issued digital currencies.” In different phrases, R3’s DCA facilitates the creation of CBDCs for central banks and deposit tokens and stablecoins for business banks, all of which might seemingly be inter-operable with different currencies on R3’s Corda community. The central financial institution element of the DCA, the CBDC accelerator, was designed particularly to fulfill CBDC specs laid out by the Financial institution of Worldwide Settlements (BIS). R3’s CBDC accelerator, in addition to what it presents for deposit tokens, permits the issuer to “outline and configure a delegated programmability framework,” which is essential provided that programmability is without doubt one of the most controversial elements of CBDCs.

One key partnership highlighting R3’s position in accelerating business banks’ forays into the digital foreign money period was cast in August 2022, when R3, together with The Depository Belief & Clearing Company (DTCC) –– a outstanding post-trade market service supplier within the world monetary companies trade — introduced the profitable launch of its Undertaking Ion platform. This non-public and permissioned Distributed Ledger Expertise (DLT) platform was developed in collaboration with key trade gamers (most of whom immediately again R3) and expertise suppliers similar to BNY Mellon, Charles Schwab, Citadel Securities, Citi, Credit score Suisse, Constancy, Goldman Sachs, J.P. Morgan, Robinhood Securities, and the State Road Company, amongst others. In 2011 alone, DTCC facilitated the settlement of the vast majority of securities transactions inside the USA and processed almost $1.7 quadrillion in transactions, solidifying its place because the world’s foremost monetary worth processor.

With the intention to greatest make the most of the approaching issuance of trillions of {dollars} in extremely regulated stablecoins, R3 bought stablecoin issuer Ivno in October 2021. This acquisition got here solely 6 months after the completion of a collateral tokenization trial Ivno had held with 18 partnered banks together with Egypt’s CIB, Singapore’s DBS, Brazil’s Itaú Unibanco, Nationwide Financial institution of Canada, Natixis, Austria’s Raiffeisen Financial institution Worldwide and US Financial institution in addition to three unnamed securities exchanges.

Invo was removed from the one potential stablecoin issuer which have partnered with R3. For example, in September 2019, Fnality and Finteum each joined forces to leverage their Utility Settlement Coin (USC) on the Corda blockchain. Fnality, headed by CEO Rhomaios Ram, the previous World Head of Product Administration for Transaction Banking at Deutsche Financial institution, identifies as a wholesale funds agency, and boasts institutional shareholders similar to Goldman Sachs, Barclays, BNY Mellon, CIBC, Commerzbank, DTCC, Euroclear, and ING, amongst others. In December 2023, Fnality, together with Lloyds Banking Group, Santander and UBS, executed the primary ever transaction settlement of digital central financial institution funds with balances of sterling utilizing an “omnibus account” on the Financial institution of England. The burden of the second was not misplaced on Hyder Jaffrey, Managing Director at UBS: “The creation of a brand new systemically essential world cost system is a as soon as in a technology occasion.”

With the DTCC’s expertise in settling the lion’s share of dollar-denominated securities, and with Fnality and Ivno’s collaborations with among the largest gamers within the worldwide banking system, R3 have quietly positioned themselves as suppliers of doubtless important infrastructure inside the imminent world system of interoperable CBDCs and their business financial institution equivalents.

R3 associate Fluent Finance, and extra particularly its UAE-based Fluent Financial Bridge, is in search of to function the connective tissue between the deposit tokens and stablecoins to be issued by business banks each within the UAE, in addition to overseas, and CBDCs by making certain their compatibility. Certainly, Fluent’s web site – in each the previous and current – has promoted its merchandise’ “CBDC financial institution compatibility.” Given Fluent’s long-standing collaboration and affiliation with R3 and the banks behind it, Fluent Financial Bridge and its stablecoin protocol have seemingly been constructed with CBDCs operating on R3’s Corda in thoughts.

As well as, simply as R3 is creating CBDCs and different digital currencies far past the UAE, Fluent can also be seeking to develop its “financial bridge” and US+ far past the Emirates. In an interview Allgood gave to R3 on January 2023, he acknowledged that Fluent has been in talks with the UAE authorities to problem a US+ equal however for his or her native foreign money, the dirham (i.e. a bank-issued dirham stablecoin that might be interoperable with its R3-developed CBDC). He additionally claimed to be far alongside in creating a US+ equal for the Mexican peso.

As well as, in the identical interview, Allgood revealed that Fluent is “seeking to do a US greenback stablecoin however with native banking in Africa” and is in talks with a number of banks throughout 36 completely different African nations in pursuit of that exact venture. Allgood, whereas busy championing and constructing an interoperable community of CBDCs throughout the globe, has begun to show Fluent’s consideration past simply US+ and in the direction of the greenback system itself.

Constructing the Digital Greenback: The Artificial Deposit Token

The US, regardless of the launch of CBDC pilots in China, Japan, Russia, India, Israel, Saudi Arabia, the UAE, and elsewhere, has but to formally launch any type of government-issued digital greenback. In a June 2023 white paper titled “Central Financial institution Digital Forex World Interoperability Ideas”, the World Financial Discussion board mirrored on the intense push by governments around the globe to discover CBDC issuance. The paper makes point out of “over 100 nations actively engaged in CBDC analysis and improvement”, whereas quoting the managing director of the Worldwide Financial Fund, Kristalina Georgieva, making the excellence that “there isn’t a common case for CBDCs as a result of every economic system is completely different”. Evidently the US has plans to be “completely different” from most nations. For example, in November 2022, two days earlier than FTX filed for chapter, Coinbase CEO Brian Armstrong was a visitor on the Circle CEO Jeremy Allaire’s podcast, and acknowledged that “each main authorities just about goes to need to have a CBDC”, whereas delineating the trail for the US would seemingly be completely different from the remainder of the world. “I believe within the US’s case, it’ll find yourself utilizing USDC [the dollar-pegged stablecoin issued by Circle] as type of like a de facto CBDC.”

Within the WEF’s white paper, two US efforts associated to CBDCs are talked about: Undertaking Hamilton, the Boston Fed’s 2020 collaboration with the Massachusetts Institute of Expertise’s (MIT) Digital Forex Initiative; and the 2022 report by The New York Fed titled Undertaking Cedar. The previous, Undertaking Hamilton, centered totally on cost throughput of a retail-facing digital foreign money, whereas the latter, Cedar, was an experiment on a deposit token to be exchanged by banks throughout wholesale settlement. The delineation between Undertaking Hamilton and Undertaking Cedar is almost equivalent to the fork within the highway presently dealing with the founding fathers of the approaching digital Federal Reserve.

In a February 2022 evaluation, Gerard DiPippo – an 11 yr veteran of the US intelligence group (particularly the CIA) who has lengthy been centered on financial points within the World South – acknowledged that:

“Greenback stablecoins have no less than one main benefit over a possible U.S. CBDC: they exist already. Even when Congress had been to resolve the Fed ought to create a CBDC, the method of improvement, experimentation, and deployment would in all probability take no less than just a few years.”

In that very same evaluation, revealed by the Nationwide Safety State-adjacent Middle for Strategic and Worldwide Research (CSIS), DiPippo added that: “The US mustn’t delay in establishing a regulatory framework to allow protected however speedy improvement of greenback stablecoins to achieve a first-mover benefit in associated funds and applied sciences.”

Certainly, simply as DiPippo famous, the digital greenback is already right here. In actual fact, it has been right here for a very long time. A Fall 2021 piece from Harvard Enterprise Evaluate made the declare that “over 97% of the cash in circulation as we speak is from checking deposits – {dollars} deposited on-line and transformed right into a string of digital code by a business financial institution.” However whereas the overwhelming majority of greenback circulation could have been diminished to 1’s and 0’s on some non-public financial institution’s spreadsheet over the previous few a long time, the belongings that truly uphold the US greenback system — US Treasuries — have developed to the digital age a bit slower. Whereas packages like TreasuryDirect do exist, wherein customers can arrange an account on-line and buy securities immediately issued by the US Division of Treasury, the precise interbank securities clearing community had remained comparatively antiquated till the launching of FedNow this previous summer season.

FedNow, on first look, appears innocuous sufficient – a brand new communications software for Federal Reserve-partnered banks to change securities. However, on second look, its necessity within the twenty first century implementation of greenback hegemony turns into clear. The settlement and change of Treasuries, the asset that truly backs the digital {dollars} created from checking deposits by non-public capital creators, has now change into additional regulated, centralized, and managed.

A reverse repo, or a reverse repurchase settlement, is the popular technique for banks to hunt yield by quickly loaning securities, particularly Treasuries, for money on account of the truth that every celebration bodily exchanges the belongings, with an settlement to repurchase the securities the following day with an added service payment. Banks a lot favor to do that versus a extra conventional mortgage construction as a result of mitigated legal responsibility danger that comes downstream of bodily holding on to the collateral within the settlement. Say a cash-strapped financial institution has just lately secured a mortgage to fulfill present liquidity wants, however earlier than they will repay the mortgage, the fruits of monetary woes causes the financial institution to declare chapter and in the end be seized by authorities. The lending financial institution not solely loses out on its service funds, but additionally the whole legal responsibility of the mortgage principal. If they’d agreed to a reverse repo change, whereas the lender would nonetheless lose out on accumulating their charges, they might no less than retain the rights to the exchanged Treasuries presently inside their custody.

The US banking system makes some huge cash by shopping for US Treasuries and utilizing them to create {dollars}. The US Division of Treasury additionally advantages because it is ready to service the price range of the US authorities by promoting its debt to the US banking system. Neither of those entities need to muck up their racket: The US authorities doesn’t need to be immediately answerable for managing retail account balances for residents (as can be the case with a direct-issued greenback CBDC), and the largest banks definitely don’t need to lose their efficient monopoly of personal capital creation by letting some outsider fintech firm safe the contract for immediately issuing digital {dollars} for the federal government. FedNow is strictly a wholesale product. In actual fact, it isn’t actually a product in any respect ––there isn’t a token and it solely goals to permit regulators to extra intently surveil the change of Treasuries.

The buying of Treasuries, nevertheless, is quickly shifting in the direction of a wholly new buyer class: stablecoin issuers. Very like how a private-sector financial institution would buy government-issued securities to again the issuance of {dollars} in a retail checking account, stablecoin issuers similar to Tether (USDT) or Circle (USDC) have change into net-buyers of short-term Treasuries known as T-bills. Tether CEO Paolo Ardoino tweeted in September 2023 that “Tether reached $72.5 billion publicity in US T-bills, being [a] high 22 purchaser globally, above the United Arab Emirates, Mexico, Australia and Spain.” Simply three months later, in December 2023, Tether’s Treasury holdings had been over $90 billion. For reference, the most important single holder of US Treasuries is Japan with simply over $1 trillion held –– Tether alone already instructions almost a tenth of their steadiness sheet. In our present excessive rate of interest surroundings, the yield from these quick period securities might be substantial, resulting in giant income streams for not solely these stablecoin issuers, however the firms and banks that custody their belongings.

Tether’s substantial Treasury holdings are distributed amongst three major custodians: Charles Schwab, Constancy and Cantor Fitzgerald. Cantor Fitzgerald is probably most well-known for having its flagship workplace destroyed in the course of the occasions of 9/11, however it continues as we speak as one of many 24 major sellers approved to commerce US authorities securities with the Federal Reserve Financial institution of New York. Earlier this month, Howard Lutnick, the CEO of Cantor Fitzgerald, made an look on CNBC Cash Movers Podcast wherein he acknowledged “I’m an enormous fan of this stablecoin referred to as Tether…I maintain their treasuries. So I preserve their treasuries, they usually have quite a lot of treasuries.” He additional acknowledged his affinity for the corporate by making reference to Tether’s latest pattern of blacklisting of retail addresses flagged by the US Division of Justice. “With Tether, you’ll be able to name Tether, they usually’ll freeze it.”

Simply this October, Tether froze 32 wallets for alleged hyperlinks to terrorism in Ukraine and Israel. In November, $225 million was frozen after a DOJ investigation alleged that the wallets containing these funds had been linked to a human trafficking syndicate. This month alone, over 40 wallets discovered on the Workplace of International Property Management’s (OFAC) Specifically Designated Nationals (SDN) Record have been frozen. Ardoino defined these actions by stating that “by executing voluntary pockets deal with freezing of recent additions to the SDN Record and freezing beforehand added addresses, we can additional strengthen the optimistic utilization of stablecoin expertise and promote a safer stablecoin ecosystem for all customers.” Only a few days in the past, Ardoino claimed that Tether has frozen round $435 million in USDT for the US DOJ, FBI and Secret Service. He additionally defined why Tether has been so keen to assist the US authorities freeze funds – Tether is in search of to change into a “world class associate” to the US to “develop greenback hegemony globally.”

The stablecoin ecosystem, the place US dollar-pegged stablecoins dominate, has change into more and more intertwined with the larger US greenback system and – by extension – the US authorities. The DOJ has the retail-facing Tether on a leash after pursuing the businesses behind it for years and now Tether blacklists accounts at any time when US authorities demand. The Treasury advantages from the mass buying of Treasuries by stablecoin issuers, with every buy additional servicing the federal authorities’s debt. The non-public sector brokers and custodians that maintain these Treasuries for the stablecoin issuers profit from the primarily risk-free yield. And the greenback itself furthers its effort to globalize at excessive velocity within the type of USDT, serving to to make sure it stays the worldwide foreign money hegemon.

In impact, Treasuries are being purchased hand over fist, and {dollars} are being spent en masse. Very like the discrepancy between Bitcoin’s UTXO or cash mannequin and Ethereum’s account steadiness mannequin, Treasuries and {dollars} behave exceptionally in another way in financial phrases. A authorities might by no means immediately problem what is named M0 –– base cash –– to retail accounts, and thus a CBDC might by no means function something however M1 — a programmable checking account that depends on belief in a monetary service supplier to be exchanged. Maybe a directly-issued US dollar-denominated CBDC is a red-herring. Simply ask the Fed.

For example, Federal Reserve Vice Chair for Supervision Michael Barr acknowledged this previous November that “There’s clearly quite a lot of innovation occurring within the non-public sector,” whereas later implying that the Federal Reserve has a “very sturdy curiosity” in regulating, approving and supervising US dollar-pegged stablecoin issuers. Deputy Secretary of the Treasury Wally Adeyemo just lately lobbied Congress on behalf of the US Treasury to increase the regulatory powers over dollar-denominated stablecoins past US firms and even US residents. “Laws might explicitly authorize OFAC to train extraterritorial jurisdiction over transactions in stablecoins pegged to the USD (or different dollar-denominated transactions) as they typically would over USD transactions,” the proposal steered, even for transactions that “contain no U.S. touchpoints.”

Final month, the Atlantic Council additionally wrote of “the present [Federal Reserve] coverage trajectory favoring non-public stablecoin issuance reasonably than official CBDC issuance,” making word of an August 8 regulation letter stating that “the Federal Reserve formally shifted its stance to advertise stablecoin issuance by banks.”

Over a yr earlier than Barr’s statements or the Atlantic Council’s put up, Bruno Sultanum, an economist within the Analysis Division on the Federal Reserve Financial institution of Richmond wrote in a July 2022 transient that “privately issued stablecoins might be equal to CBDCs” and that “there could also be a pathway to create an efficient ‘artificial’ CBDC within the type of stablecoins. Extra typically, the discussions across the introduction of CBDCs ought to at all times embody an analysis of the potential for contemplating well-regulated stablecoins as a viable (and probably preferable) various.”

As well as, the aforementioned CSIS transient authored by CIA veteran DiPippo mentions a number of architectures the US authorities might undertake for his or her digital greenback, whereas realizing some great benefits of a bank-issued deposit token. “An artificial CBDC, will not be actually a CBDC in any respect, as a result of the central financial institution wouldn’t be issuing the digital foreign money. An artificial CBDC is a stablecoin with a twist: the issuing monetary establishment would again its stablecoin with reserves on the Fed.” He then famous that “An artificial CBDC, or a system allowing the issuance of a number of absolutely backed greenback stablecoins, can be as protected as a CBDC whereas providing extra private-sector competitors and innovation.” In November 2021, the President’s Working Group on Monetary Markets (PWG), the Federal Deposit Insurance coverage Corp. (FDIC) and the Workplace of the Comptroller of the Forex (OCC) launched a joint report on stablecoins, which highlighted that stablecoins might enhance the US cost system however might additionally create monetary dangers if left unregulated. Typically, realizing any advantages from stablecoins would require authorities regulation.

In ready remarks this October, Barr acknowledged “analysis is presently centered on end-to-end system structure, similar to how ledgers that document possession of and transactions in digital belongings are maintained, secured, and verified, in addition to tokenization and custody fashions.” Barr additionally made the declare that any USD-denominated token “borrows the belief of the central financial institution,” and thus “the Federal Reserve has a powerful curiosity in making certain that any stablecoin choices function inside an acceptable federal prudential oversight framework, so they don’t threaten monetary stability or funds system integrity.” Because of the reputation of and quantity current in each the Treasury and stablecoins markets, there are presently many non-public banks trying to digitize the securities market by creating an artificial deposit token that acts like Treasuries.

As well as, the latest push within the US towards regulated stablecoins/deposit tokens and away from a direct-issued CBDC has different motives. Whereas this push is no less than partially motivated by the “unhealthy fame” that the time period stablecoin has developed within the aftermath of the TerraLuna fraud in early 2022 and subsequent scandals within the crypto trade, business banks – together with people who again Fluent Finance, R3 and their equivalents – need to problem the stablecoins/deposit tokens themselves so as to proceed fractional reserve banking.

Fractional reserve banking, lengthy controversial on account of its position in facilitating financial institution runs and financial institution insolvency and characterised as some as little greater than embezzlement, has lengthy been a cornerstone of the US banking system. Nonetheless, the present stablecoin paradigm, together with that previously embraced by Fluent Finance, have fallen out of favor with business banks because the 1:1 peg signifies that banks must maintain onto equal reserves for each coin/token issued. In fractional reserve banking, banks interact in “credit score creation” by loaning out the majority of the cash deposited by its prospects and are unable to instantly (and even shortly) redeem prospects’ cash upon request – the whole function of the 1:1 ratio that characterizes most of as we speak’s stablecoins. For banks to proceed “enterprise as regular”, the issuance of stablecoins and deposit tokens should come underneath their purview, versus current stablecoin issuers and even the Fed. Fluent Finance, as an organization closely influenced and guided by highly effective business banks, is clearly positioning itself to be a key a part of this bank-led digital greenback system.

In January 2023, Fluent’s Bradley Allgood instructed CoinDesk how the USA has been establishing its choice for a private-public mannequin. He particularly pointed to the Federal Reserve Financial institution of New York and highlighted its initiatives in testing deposit tokens backing digital {dollars} for wholesale transactions in collaboration with main banks:

“While you have a look at the Fed of New York and what they’ve been doing of their innovation places of work, this has been setting the usual, with all of it leaning in the direction of wholesale, tokenized deposits or tokenized legal responsibility community settlement between financial institution to financial institution.”

Throughout a lot of 2022, and significantly the timeframe wherein Fluent Finance was forging its early partnerships together with with Farmington/Moonstone, the behind-the-scenes push to create an artificial CBDC for the US greenback within the type of regulated dollar-pegged stablecoins and/or deposit tokens was properly underway. Fluent, from its earliest days, has sought to develop this artificial CBDC and make it interoperable with any future direct-issued CBDC from the Federal Reserve whereas additionally exporting this artificial greenback CBDC to the World South. In mild of the corporate’s (and US+’s) trajectory, it now is sensible to revisit the more than likely motivation behind Moonstone’s partnership with Fluent previous to FTX’s collapse in addition to the seemingly actual objective behind Farmington’s transition into Moonstone.

The Bankman-Fried Stablecoin That Virtually Was

Previous to the collapse of the Sam Bankman-Fried-led change FTX, there was already appreciable hypothesis concerning the uncommon relationship between FTX and its subsidiaries, Deltec and the dollar-pegged stablecoin Tether (USDT). For example, almost a yr earlier than FTX went underneath, Protos reported that “over two-thirds of all Tether minted throughout a number of years went to only two crypto firms”, one in all which was the FTX-linked Alameda Analysis, the identical Alameda Analysis that might later pour thousands and thousands into Farmington State Financial institution throughout its suspect transition into Moonstone. Earlier that yr, Alameda government Sam Trabucco primarily admitted on Twitter that Alameda would use its huge holdings of USDT to take care of USDT’s peg to the US greenback (one thing additionally admitted by former FTX government Ryan Salame). By October of 2021, Alameda had been issued virtually $37 billion price of USDT and had instantly forwarded $30 billion of that to FTX. Round that very same time, FTX issued a $50 million mortgage to Deltec, which was a key financial institution for FTX and nonetheless is for Tether and whose chairman, Jean Chalopin, had just lately acquired Farmington State Financial institution.

Over the following a number of months, Alameda Analysis and Sam Bankman-Fried himself would pour many thousands and thousands into the Chalopin-controlled entity, making Farmington/Moonstone the latest entity of the Deltec-FTX-Tether nexus. This brings us to the massive query: If Deltec and FTX had been so near Tether, why was the financial institution they managed – Farmington/Moonstone – in search of to associate so intimately with one other US dollar-pegged stablecoin – Fluent Finance’s US+?

For a number of years, and now greater than ever, Tether has been underneath heavy scrutiny from US authorities, significantly the DOJ, and – given the US authorities’s push for regulated stablecoins/deposit tokens in lieu of a direct problem CBDC – it’s doable that Tether could not make the lower as soon as these laws lastly come into drive (although Tether’s latest overtures to US authorities and Congress clearly search to stop that). Tether, together with Deltec and fairly clearly FTX, have lengthy been suspected of participating (or in FTX’s case, confirmed to have engaged) in financial institution fraud and a collection of illicit monetary actions. It appears as if highly effective forces deeply tied to Tether, particularly Chalopin and Bankman-Fried, had been in search of to make use of Moonstone and its partnership with Fluent’s US+ the way in which the FTX internet of firms/banks had used Tether. This could have presumably allowed them to proceed their identical shady monetary machinations underneath the approaching regulatory paradigm.

Notably, in late October 2022, three days after the Chalopin/Bankman-Fried-affiliated Moonstone partnered with Fluent Finance, Sam Bankman-Fried acknowledged that FTX was on account of announce the now bankrupt change’s collaboration with an unspecified stablecoin “within the not-too-distant future.” One wonders if the thousands and thousands in political donations made by Bankman-Fried (and doubtlessly these made by FTX government Ryan Salame) in 2022 had been geared toward wooing politicians to favor the deliberate FTX-affiliated stablecoin as a frontrunner for the approaching “digital greenback” paradigm.

In different phrases, the objective was apparently to have the identical group of actors transition from the “untrusted” Tether stablecoin to the “trusted” US+ stablecoin. The truth that Fluent Finance, whose co-founders embody the alleged inventor of CBDCs and which was closely influenced from the beginning by highly effective business banks, claims to be a “reliable” various to Tether is deeply undermined and admittedly unbelievable provided that they might agree to permit the identical untrustworthy actors deeply concerned in Tether’s questionable minting actions (and FTX’s brazen fraud) to mint their “regulatory compliant” and “trusted” US+ stablecoin.

The Public-Non-public Digital Greenback

Following the collapse of FTX, and later Moonstone, Fluent Finance has continued in pursuit of its final objective – to create a “trusted” stablecoin and stablecoin protocol on behalf of the business banking giants it was at all times meant to serve. In a September 2023 op-ed for Cointelegraph tellingly entitled “CBDCs might assist a extra secure economic system – if banks run the present,” Allgood made his allegiances clear. In that article, Allgood writes that “using CBDCs in an try and undercut, circumvent or cannibalize the whole business banking sector is as a lot a pipe dream for effectivity maximalists as it’s a recipe for failure.” “Business banking is not going to be left at the hours of darkness ages,” he additionally claims.

In his protection of the business financial institution establishment, Allgood got here out in opposition to the present stablecoin paradigm in a latest interview with the IB Occasions, talking in favor of bank-issued and controlled stablecoins backed by deposit tokens. “Stablecoins haven’t panned out the way in which most anticipated three years in the past.” In line with Allgood, deposit token fashions are actually “rising from the pack” of current stablecoin issuance because the “most promising stable-valued digital belongings.” He goes on to politically make clear that “stablecoins should not the unhealthy guys…simply the very best effort from a earlier period.” On this interview and likewise the Cointelegraph article, Allgood makes it clear that Fluent Finance not solely possesses the mandatory digital infrastructure, but additionally the institutional connections to maintain non-public capital creation within the palms of business banks through deposit token structure.

Allgood additionally instructed the IB Occasions that “the sticking level with stablecoins is that their issuers are primarily lean startups…When you think about the inherent safety dangers, frequent depeggings and compliance points, it’s not obscure why stablecoins have had no success by any means selecting up traction in conventional use case eventualities.” The argument for transferring the reserves of stablecoins again into the palms of the US banking system underneath the guise of additional stability appears logical solely till one remembers that Allgood’s favored custodians are the fractional reserve banking trade –– who would have the ability to interact on this controversial apply at a a lot bigger scale underneath this new paradigm. Banking the unbanked –– a standard trope from the stablecoin trade –– additionally sounds good in idea, so long as you ignore who will get to truly do the banking.

“If all goes properly,” claims Allgood, “the worldwide adoption of CBDCs will marshal a brand new monetary paradigm the place central banks implement superior financial coverage on the wholesale stage whereas permitting business banks to do what they do greatest on the retail stage with stablecoins and deposit tokens.”

Whereas many rightly concern the hazard to particular person freedoms introduced by government-issued CBDCs, this isn’t the paradigm being introduced into focus by former Moonstone associate Fluent Finance or different key actors in constructing out the way forward for government-approved digital currencies. As an alternative of giving central bankers full management over your funds when it comes to surveillance and programmability, it is going to be the massive Wall Road banks –– who within the US, personal the Fed anyway – that can do the programming and surveilling. The additional blurring of the private and non-private banking sector stays a robust software of obfuscation for the digital greenback system to skirt constitutional violations of buyer rights within the type of warrantless asset seizure and information harvesting by a non-public sector that absolutely collaborates with the general public sector. The digitization of the greenback, and the Treasuries that again them, leverage the databases of blockchains to not solely reveal reserves of deposits, but additionally to trace the customers of the system. “The FX settlement course of wants elevated transparency and traceability”, R3 CEO David Rutter as soon as defined. Rutter then boasted that his firm “is match to ship on each counts.”

The simulated concern of governments and central banks programming your foreign money to run out shall be conveniently eased by a public rejection of a directly-issued CBDC within the US by the Fed. The upholders of the established order hope that the realities of this false victory, and the stablecoin/deposit token system to be applied in lieu of a direct-issue digital greenback, will go unnoticed by the American public, significantly these segments of the inhabitants already cautious of CBDCs. No matter excuse or justification is given to maneuver the US – and far of the world – into this new monetary paradigm, relaxation assured that the identical outdated bankers and corporations – together with those that got here underneath scrutiny as a part of the FTX scandal – is not going to solely keep, however achieve, unprecedented management over the monetary exercise and habits of each American and whoever else they resolve to dollarize.