Software program firm Palantir Applied sciences (NYSE: PLTR) and chip firm Nvidia (NASDAQ: NVDA) are two of the most well liked shares on Wall Road. Each shares are up over 240% over the previous 12 months and have fierce loyalty amongst traders.

Is one synthetic intelligence (AI) inventory higher than the opposite? To search out out, I in contrast them head-to-head to see why they’re thriving and whether or not they can proceed. It was a really shut race, however one stood out simply forward of the opposite.

Here’s what you should know.

Assembly these two very totally different firms

Each shares soared because of the implausible efficiency of their underlying companies. Nevertheless, these two AI firms are very totally different. Nvidia spent years specializing in high-performance GPUs, which grew to become splendid for knowledge facilities and AI. Nvidia’s high-quality merchandise and CUDA software program, which helps prospects effectively use their GPUs energy, have led to Nvidia grabbing an early stranglehold on the AI chip market — an estimated 80% to 90%.

Alternatively, Palantir builds customized software program purposes for each authorities and business purposes. It runs three software program platforms: Gotham, Foundry, and AIP for AI purposes. You possibly can consider Palantir as an working system that helps organizations use their knowledge. The corporate’s intent is that it augments human intelligence; it would not exchange it.

A better take a look at every firm’s progress

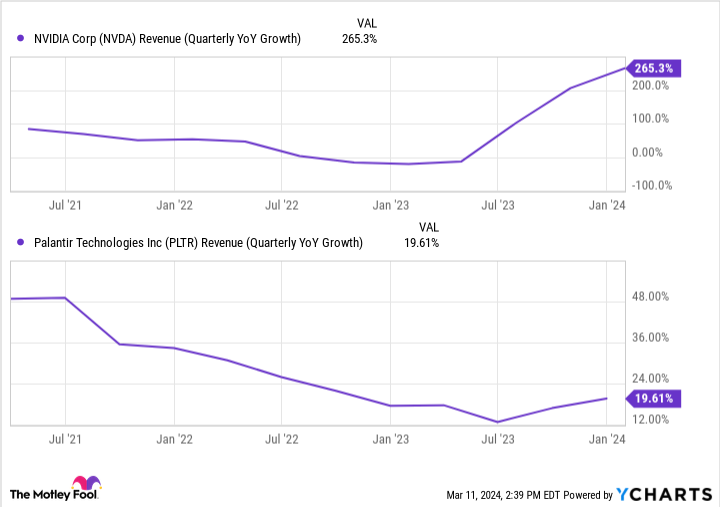

From a pure numbers standpoint, Nvidia is rising leaps and bounds sooner than Palantir. You possibly can see beneath how each firms started accelerating income progress in mid-2023, however Nvidia soared on huge knowledge middle spending from large expertise prospects, primarily within the “Magnificent Seven.” It could possibly be honest to surprise how lengthy this monumental increase in knowledge middle spending from large tech will proceed.

One chance is that these firms begin producing customized chips in-house, weaning themselves off of Nvidia’s. That would damage long-term progress for a corporation at the moment getting most of its income from a small handful of consumers.

Talking of Palantir, the corporate will not be as explosive as Nvidia. However what impresses me is the corporate’s increasing buyer base. Palantir’s U.S. buyer rely grew 55% 12 months over 12 months within the fourth quarter and 22% quarter over quarter. Clients are available all styles and sizes, so it isn’t a exact translation. Such buyer progress bodes properly for long-term income progress.

Possibly Nvidia’s buyer focus will not matter, and Nvidia’s chips will keep their market share. Nonetheless, I might prefer to see buyer enlargement like Palantir’s.

What is the higher bang to your buck?

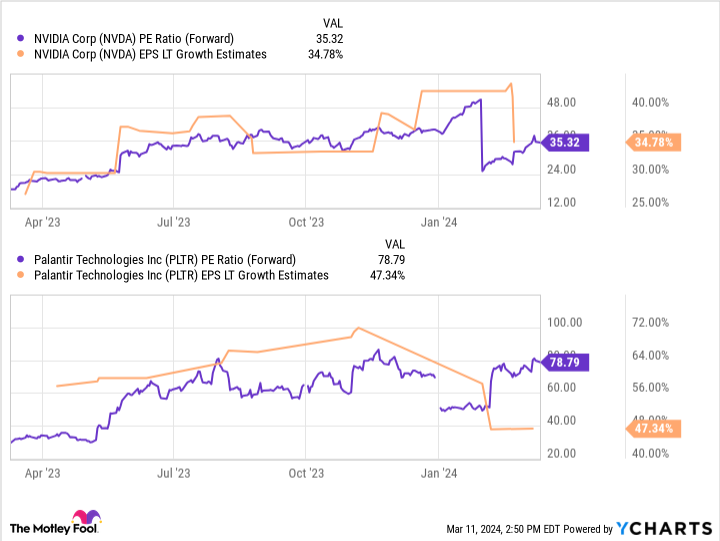

Analysts count on vital earnings progress from each firms transferring ahead. On a ahead foundation, that makes each shares cheaper than you’d guess after each of their 200% runs. I like utilizing the PEG ratio to match how a lot I pay for a corporation’s earnings progress. The decrease the PEG ratio, the higher, and I wish to spend beneath 1.5 if I can.

Nvidia suits that standards with a PEG ratio of simply over 1. Palantir would not fairly match, with its PEG ratio of 1.6.

Nvidia is handily the higher worth right now, primarily based on every firm’s anticipated long-term earnings progress. After all, the caveat is whether or not every firm will carry out as much as expectations.

The decision is…

Each firms are glorious AI shares and leaders of their respective areas. Each are accelerating their income progress. Naturally, analysts are very optimistic about every firm’s earnings progress transferring ahead. Whichever firm you imagine is extra prone to meet progress expectations over the subsequent three to 5 years might be your winner.

This Idiot is giving Palantir a slight edge. Why?

Palantir will get roughly half its income from authorities contracts. The corporate’s lengthy historical past with the federal government might put a little bit of a ground into Palantir’s enterprise, plus the upside from increasing its buyer base. In the meantime, Nvidia’s buyer focus could possibly be problematic if a major buyer opts for one more chip.

Whereas the numbers say Nvidia is the higher purchase, there’s an argument that traders can belief Palantir’s long-term progress barely extra, particularly when taking a look at the long run.

Do you have to make investments $1,000 in Palantir Applied sciences proper now?

Before you purchase inventory in Palantir Applied sciences, think about this:

The Motley Idiot Inventory Advisor analyst group simply recognized what they imagine are the 10 finest shares for traders to purchase now… and Palantir Applied sciences wasn’t one in every of them. The ten shares that made the minimize might produce monster returns within the coming years.

Inventory Advisor supplies traders with an easy-to-follow blueprint for achievement, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than tripled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of March 11, 2024

Justin Pope has no place in any of the shares talked about. The Motley Idiot has positions in and recommends Nvidia and Palantir Applied sciences. The Motley Idiot has a disclosure coverage.

Higher Synthetic Intelligence (AI) Inventory: Palantir vs. Nvidia was initially printed by The Motley Idiot