Many revenue traders focus primarily on an organization’s observe file for making and elevating dividend funds, and the dividend yield. However if you happen to’ve been questioning which firms pay essentially the most dividends, you have come to the appropriate place.

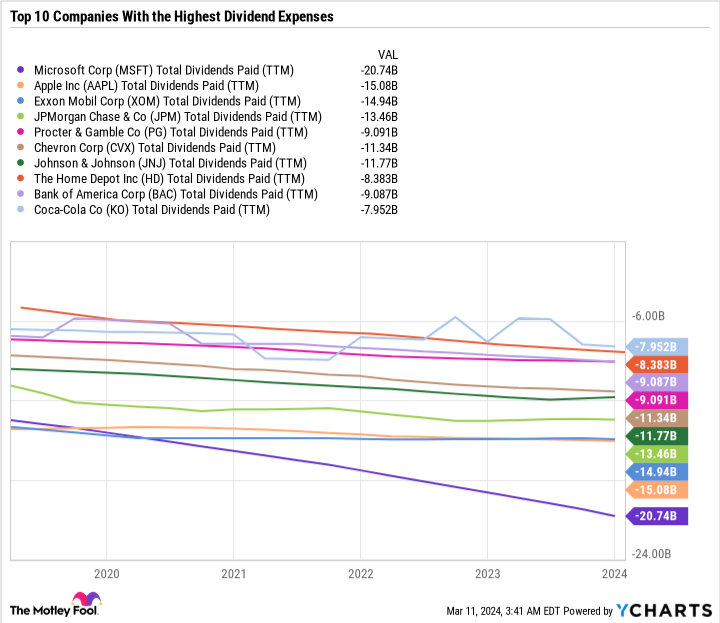

The highest candidates could be massive firms with excessive yields, however the two firms with the best dividend bills are literally Microsoft (NASDAQ: MSFT) and Apple (NASDAQ: AAPL) — each “Magnificent Seven” shares.

This is a take a look at the ten U.S.-based firms with the most important dividend bills, why Microsoft leads the group, and why Microsoft is price shopping for now.

Microsoft’s multibillion-dollar annual dividend hikes

Aside from ExxonMobil and Financial institution of America, the ten U.S. firms with the most important dividend bills are all within the Dow Jones Industrial Common, which is understood for having industry-leading firms as its elements.

In the event you observe the purple line within the chart, you will see that Microsoft’s dividend cost has elevated considerably, particularly just lately. In truth, it has almost doubled during the last six years. For fiscal 2024, Microsoft elevated its dividend by greater than 10%. As a result of it’s such a big firm, every 5% enhance within the dividend interprets to round $1 billion extra in dividend bills.

In the meantime, Apple has made naked minimal dividend raises of 1 cent per share per yr for the previous few years. Apple prefers to return cash to shareholders through inventory buybacks moderately than with dividends.

Do not underestimate Microsoft’s dividend

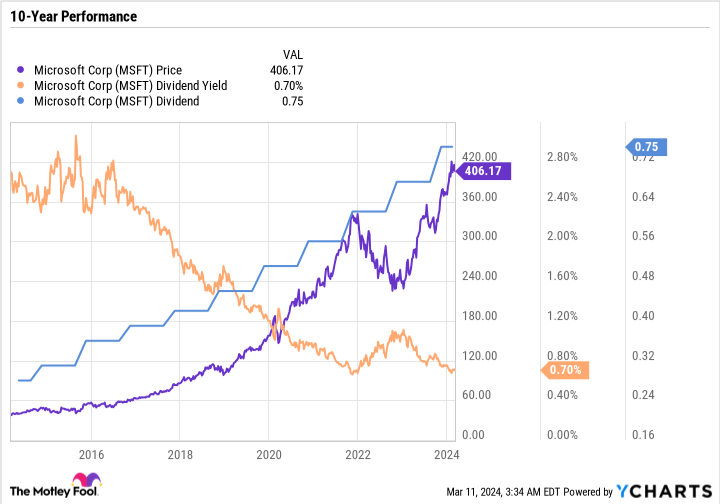

Microsoft has a below-average yield of simply 0.7% — however that is nonetheless essentially the most of any Magnificent Seven inventory, even when factoring in Meta Platforms‘ new dividend.

Microsoft has made sizable dividend hikes, however its inventory value progress has effectively outpaced that dividend progress price, which has resulted in a shrinking yield over time. Over the past decade, administration has almost tripled the dividend, but the yield has fallen from greater than 2.5% to 0.7% merely due to the inventory’s monster 900% acquire over that point.

In the event you’re seeking to construct passive revenue streams for the lengthy haul, then an organization’s capability and willingness to lift its dividend will show extra essential than its present yield. Microsoft stands out as a result of it may afford to lift its dividend commonly, purchase again inventory, fund its operations, spend money on analysis and growth, and nonetheless preserve a stability sheet with additional cash than debt.

Basically, Microsoft can do all of it. It is higher to view its dividend as a cherry on high of its funding thesis as a substitute of it in isolation.

Constructing an funding thesis

There are three primary methods an organization can reward its shareholders — capital good points, dividends, and inventory repurchases. When contemplating whether or not to spend money on a inventory, it is essential to know which of these levers the corporate is most targeted on pulling.

For a lot of firms, it is all about capital good points. Amazon and Tesla, for instance, slot in that class: They do not pay dividends and have massive stock-based compensation applications, which enhance their excellent share counts and dilute their current shareholders.

For a stodgy dividend-payer like Procter & Gamble, dividends and buybacks are arguably an even bigger a part of the funding thesis than potential share value good points. Though P&G can nonetheless shock to the upside — the inventory is up by greater than 9% yr so far and is thrashing the S&P 500.

Then there are the uncommon firms that each have loads of room to develop and likewise reward their shareholders with buybacks and dividends. Microsoft is on this elite class. Over the past 5 years, the corporate has diminished its share depend by 3%, raised its dividend by 63%, and its inventory value is up by greater than 255%. It has delivered the trifecta for shareholders.

Leveraging AI throughout enterprise channels

Microsoft stands out as one of the well-rounded buys within the inventory market proper now as a result of it’s a comparatively low-risk however excessive potential-reward firm. With such excessive money circulate and a robust stability sheet, Microsoft can afford to make errors, fund acquisitions, attempt one thing new, and take dangers at occasions when many different firms lack the capital or market place to take action. Microsoft additionally has a transparent path towards monetizing synthetic intelligence (AI). It has a number of high-margin enterprise models which can be associated however nonetheless diversified.

Microsoft Copilot is an AI assistant that works throughout a number of functions, amongst them the Microsoft 365 applications and GitHub. On Microsoft’s fiscal 2024 second-quarter earnings name, administration went into element in regards to the many ways in which Copilot helps its prospects save time and drive effectivity, and it is contributing to the underside line.

Even when Copilot hits a snag and its affect on progress throughout all these merchandise seems to be restricted, it isn’t the corporate’s solely AI play. There’s additionally Azure AI for Microsoft’s Clever Cloud section, which serves a very totally different {industry} than Copilot targets.

In sum, Microsoft’s AI aspirations do not hinge on a single product or thought. AI is already boosting the corporate’s profitability and contributing to progress, and there is not any purpose to consider that development will decelerate anytime quickly.

Anticipate that to supply a snowball impact. Microsoft may select to speed up its share value progress, return capital to shareholders via bigger buybacks, or elevate its dividend at a sooner price. Traders stand to profit regardless of which lever Microsoft chooses to drag.

Microsoft sports activities a premium valuation for good causes

The one challenge with Microsoft is its valuation. It trades at a 36.8 price-to-earnings (P/E) ratio, which is effectively above its historic common and the S&P 500’s 27.8 common P/E ratio. The inventory is not low cost, which reveals that traders have already got excessive expectations for Microsoft.

Do not count on Microsoft’s valuation enlargement to proceed. The good points must be pushed by earnings, which is not a foul factor. It simply means a number of the “simple cash” has already been made.

The excellent news is that Microsoft has a multidecade runway for rising earnings and rewarding its shareholders. Even with the inventory’s costly price ticket, Microsoft stands out as one of many safer methods to spend money on AI and acquire some passive revenue within the course of.

The place to speculate $1,000 proper now

When our analyst group has a inventory tip, it may pay to hear. In spite of everything, the publication they’ve run for twenty years, Motley Idiot Inventory Advisor, has greater than tripled the market.*

They simply revealed what they consider are the 10 greatest shares for traders to purchase proper now… and Microsoft made the listing — however there are 9 different shares you could be overlooking.

*Inventory Advisor returns as of March 11, 2024

JPMorgan Chase is an promoting companion of The Ascent, a Motley Idiot firm. Financial institution of America is an promoting companion of The Ascent, a Motley Idiot firm. John Mackey, former CEO of Entire Meals Market, an Amazon subsidiary, is a member of The Motley Idiot’s board of administrators. Daniel Foelber has no place in any of the shares talked about. The Motley Idiot has positions in and recommends Amazon, Apple, Financial institution of America, Chevron, House Depot, JPMorgan Chase, Microsoft, and Tesla. The Motley Idiot recommends Johnson & Johnson and recommends the next choices: lengthy January 2026 $395 calls on Microsoft and brief January 2026 $405 calls on Microsoft. The Motley Idiot has a disclosure coverage.

Meet the “Magnificent Seven” Inventory That Pays Extra Dividends Than Any Different U.S.-Primarily based Firm was initially printed by The Motley Idiot