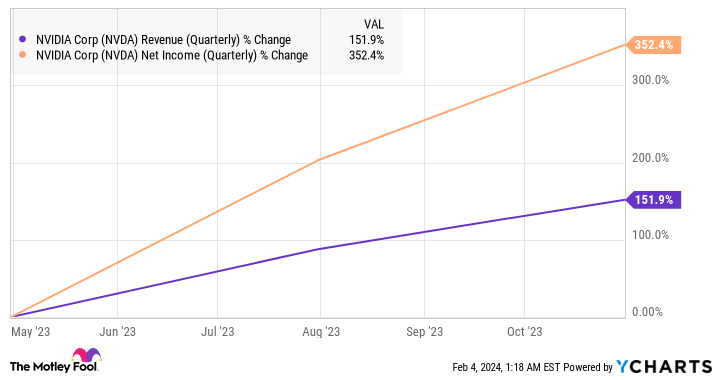

The factitious intelligence (AI) gravy prepare has given a number of shares a giant enhance over the previous yr, notably Nvidia, which has capitalized on the booming demand for AI chips and loved an eye-popping bounce in its income and earnings. Shares of Nvidia have shot up a terrific 215% up to now yr.

Because the chart reveals, the inventory’s surge is justified, contemplating how quickly its income and earnings have elevated in current quarters.

Nevertheless, the massive bounce in worth signifies that shares of Nvidia should not in worth territory anymore. Nvidia sports activities a surprising price-to-sales ratio of 37. It additionally trades at a lofty 90 occasions trailing earnings, which is larger than its five-year common of 79.

In fact, Nvidia can justify these costly multiples by sustaining its strong development sooner or later, however there are cheaper choices to capitalize on the AI wave as nicely. Tremendous Micro Pc (NASDAQ: SMCI) and Qualcomm (NASDAQ: QCOM) are two attractively valued shares that you could be contemplate shopping for proper now.

1. Tremendous Micro Pc

Tremendous Micro Pc is already in red-hot type on the inventory market, surging a whopping 587% up to now yr and crushing Nvidia’s returns by an enormous margin. Nevertheless, shares of the corporate that is identified for making AI server and storage options proceed to commerce at very enticing ranges regardless of this enormous bounce.

You should buy Tremendous Micro inventory for simply 3.3 occasions gross sales proper now. Shopping for the inventory at this valuation seems to be like a no brainer, not solely as a result of it’s manner cheaper than Nvidia, but in addition as a result of it’s rising at an amazing tempo.

Tremendous Micro launched its fiscal 2024 second-quarter outcomes (for the three months ended Dec. 31) on Jan. 29. The corporate’s income greater than doubled from the year-ago interval to $3.66 billion final quarter. Its non-GAAP (usually accepted accounting ideas) web revenue shot up from $3.26 per share within the year-ago interval to $5.59 per share.

The corporate’s spectacular income and earnings development was pushed by the fast deployment of AI servers. Tremendous Micro has optimized its server options in line with the necessities of AI servers, serving to knowledge middle operators scale back electrical energy and cooling prices. Its server rack options are used for deploying AI chips from a number of distributors equivalent to Nvidia, Intel, and Superior Micro Gadgets.

The great half is that the corporate is witnessing terrific demand for its choices, which is why it has been targeted on enhancing its manufacturing capability. Charles Liang, CEO of Tremendous Micro, identified on the corporate’s newest earnings convention name:

At this time, our manufacturing utilization charge is about 65% throughout our USA, Netherlands, and Taiwan services, and they’re shortly filling. To deal with this fast capability problem, we’re including two new manufacturing services and warehouses close to our Silicon Valley HQ, which can be working in a number of months. The brand new Malaysia facility will give attention to increasing our constructing blocks with decrease prices and elevated quantity, whereas different new websites will assist our annual income capability above $25 billion.

It will not be stunning to see Tremendous Micro ultimately hitting $25 billion in annual income because of its capability growth strikes, as demand for AI servers is predicted to develop fivefold between 2023 and 2027, producing an annual income of $150 billion on the finish of the forecast interval.

Extra importantly, Tremendous Micro is already benefiting from this strong development in AI server demand, as its newest steering replace tells us. The corporate now expects to finish fiscal 2024 with income of $14.5 billion on the midpoint of its steering vary, which might be a 106% bounce over the prior yr. Tremendous Micro was earlier anticipating fiscal 2024 income to land at $10.5 billion.

Assuming Tremendous Micro does hit its annual income steering and maintains its gross sales a number of, its market capitalization may enhance to $48 billion. That will be a 50% bounce from present ranges, which is why buyers wanting so as to add an AI inventory to their portfolios ought to contemplate performing shortly earlier than Tremendous Micro heads larger.

2. Qualcomm

Share of Qualcomm have underperformed the broader market over the previous yr with good points of simply 5%, which isn’t stunning, contemplating the cell chipmaker’s tepid monetary efficiency.

Qualcomm has been weighed down by poor smartphone gross sales up to now yr. Based on market analysis agency IDC, smartphone shipments had been down 3.2% in 2023 to 1.17 billion items. Qualcomm will get greater than two-thirds of its whole income from promoting chipsets utilized in smartphones, so the weak spot on this phase was certain to have a damaging influence on the corporate’s efficiency.

The excellent news for Qualcomm is that the smartphone market is about for a strong turnaround from 2024. The turnaround is already underway, with smartphone shipments rising 8.5% within the fourth quarter of 2023, outpacing the 7.3% development that analysts had been in search of.

Morgan Stanley is anticipating the worldwide smartphone market to develop by 4% in 2024 and 4.4% subsequent yr. Nevertheless, the tempo of development in This autumn 2023 factors towards higher smartphone gross sales development this yr, with AI anticipated to play a central position in driving a stronger efficiency.

Counterpoint Analysis estimates that shipments of generative AI-powered smartphones may hit 100 million items in 2024. Annual shipments of AI-enabled smartphones are anticipated to hit 522 million items in 2027, clocking an annual development charge of 83%.

In all, a complete of 1 billion AI-powered smartphones are anticipated to be shipped over the subsequent 4 years. Qualcomm is already on its strategy to capitalizing on this chance, with its Snapdragon 8 Gen 3 chip powering AI options on Samsung‘s newest Galaxy S24 Extremely smartphone. Qualcomm’s administration identified on the newest earnings convention name that Samsung’s S24 household of units contains “on-device AI options equivalent to stay translate interpreter, chat help, nightography, and extra.”

Moreover, Qualcomm has “prolonged a multi-year settlement with Samsung regarding Snapdragon platforms for flagship Galaxy smartphone launches beginning in 2024.” This could pave the best way for Qualcomm to benefit from the nascent AI-enabled smartphone market in the long term, contemplating that Samsung is the world’s second-largest smartphone producer.

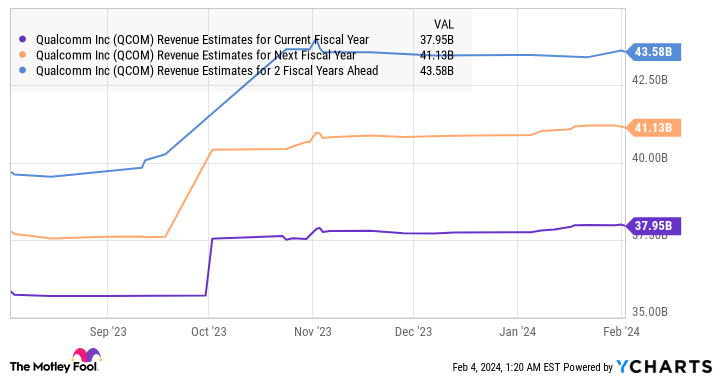

It’s price noting that analysts have already been elevating Qualcomm’s income development estimates of late.

AI may give the corporate an extra raise and assist Qualcomm outpace analysts’ expectations sooner or later. However even when the corporate hits $44 billion in annual income over the subsequent couple of years and maintains its present gross sales a number of of 5, its market capitalization may bounce to $220 billion. That will be a 39% enhance over present ranges.

Nevertheless, do not be shocked to see Qualcomm inventory delivering stronger good points on the again of a sooner bounce in its income. Furthermore, the market might reward it with the next gross sales a number of based mostly on its AI prospects, which is why savvy buyers would do nicely to purchase the inventory now.

Must you make investments $1,000 in Tremendous Micro Pc proper now?

Before you purchase inventory in Tremendous Micro Pc, contemplate this:

The Motley Idiot Inventory Advisor analyst staff simply recognized what they consider are the 10 greatest shares for buyers to purchase now… and Tremendous Micro Pc wasn’t one in every of them. The ten shares that made the minimize may produce monster returns within the coming years.

Inventory Advisor gives buyers with an easy-to-follow blueprint for fulfillment, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than tripled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of February 5, 2024

Harsh Chauhan has no place in any of the shares talked about. The Motley Idiot has positions in and recommends Superior Micro Gadgets, Nvidia, and Qualcomm. The Motley Idiot recommends Intel and Tremendous Micro Pc and recommends the next choices: lengthy January 2023 $57.50 calls on Intel, lengthy January 2025 $45 calls on Intel, and quick February 2024 $47 calls on Intel. The Motley Idiot has a disclosure coverage.

Missed Out on Nvidia? 2 Extremely Low-cost Synthetic Intelligence (AI) Shares to Purchase Earlier than They Skyrocket 39% to 50%. was initially printed by The Motley Idiot