It looks like everybody and their uncle hate Intel (NASDAQ:INTC) immediately. This can be a signal of how fickle the market may be, however I encourage you to take a look at the massive image and make your personal choices. When the mud settles shortly, I count on the market to understand Intel once more, and for the long run, I’m bullish on INTC inventory.

Intel is a chipmaker that, not like a number of the firm’s rivals, really manufactures its personal microchips. Having a foundry enterprise is dangerous, little question, however it’s what units Intel aside.

Right this moment’s INTC inventory dumpage is a textbook instance of how investor sentiment can activate a dime. In only a yr’s time, Intel has gone from doghouse to darling and again. Don’t be annoyed on the market’s wild temper swings, although, since irrational conduct results in volatility, and volatility results in alternative.

The Good Information That No One is Speaking About

INTC inventory is down 12% immediately, despite the fact that there are a number of constructive information gadgets to report. In impact, the market is so hyper-focused on Intel’s quarterly report and ahead steering that it’s fully overlooking some necessary developments regarding Intel.

To start with, Intel simply celebrated the opening of the corporate’s manufacturing facility in Rio Rancho, New Mexico. In keeping with Keyvan Esfarjani, Intel govt vice chairman and chief international operations officer, this represents the “opening of Intel’s first high-volume semiconductor operations and the one U.S. manufacturing facility producing the world’s most superior packaging options at scale.”

Moreover, Intel introduced a collaboration with Taiwan-based United Microelectronics Company (NYSE:UMC) to develop a “12-nanometer semiconductor course of platform to handle high-growth markets similar to cellular, communication infrastructure and networking.” It’s attention-grabbing that Intel is partnering with a Taiwanese foundry enterprise like United Microelectronics Company.

With this Taiwan-based partnership, may Intel and UMC be poised to steal vital market share from Taiwan Semiconductor (NYSE:TSM)? It’s a query that should be thought-about, however hardly anybody’s eager about it immediately.

The Market Can’t Tolerate Cautious Steering

To be blunt, the market is so spoiled that it received’t tolerate something however a full-on beat-and-raise anymore. Generally, there’s a beat-and-raise, however the earnings beat and/or the steering elevate isn’t excessive sufficient to impress buyers. It’s an odd phenomenon – however once more, irrationality results in alternative.

With its outcomes for the fourth quarter of Fiscal Yr 2023, Intel positively achieved the “beat” a part of the beat-and-raise method. Intel CEO Pat Gelsinger had each proper to boast, saying, “We delivered sturdy This autumn outcomes, surpassing expectations for the fourth consecutive quarter with income on the greater finish of our steering.”

Right here’s the rundown. Intel’s quarterly income grew by 10% year-over-year to $15.4 billion, beating analysts’ consensus expectations by $230 million. Furthermore, Wall Avenue referred to as for Intel to put up Fiscal This autumn-2023 earnings of $0.45 per share, however the firm really earned $0.54 per share.

After INTC doubled from $24 and alter to $50, you would possibly assume that Intel’s Avenue-beating quarterly outcomes would ship the share value greater. But, Intel didn’t ship the “elevate” a part of the beat-and-raise combo that individuals count on these days.

Particularly, Intel offered a current-quarter income steering vary of $12.2 billion to $13.2 billion, whereas analysts’ consensus forecast referred to as for $14.2 billion in income. As well as, whereas Wall Avenue forecast adjusted Fiscal Q1-2024 earnings of $0.32 per share, Intel’s administration solely guided for $0.13 per share.

In gentle of this, a variety of analysts have turned cautious on INTC inventory. Two examples are Bernstein’s Stacy Rasgon and Stifel Nicolaus’s Ruben Roy, who not too long ago printed Maintain/Impartial scores on Intel shares. Moreover, Rasgon’s $42 value goal and Roy’s $45 value goal aren’t notably optimistic.

Give it some thought – Intel inventory must go virtually nowhere for the following 12 months so as to land at these value targets. But, the corporate’s outcomes reveal that Intel is able to surpassing Wall Avenue’s monetary estimates. Now that the current-quarter expectations are fairly low, don’t be too stunned if there’s one other earnings beat coming — although I can’t assure a beat-and-raise, which everyone appears to demand now.

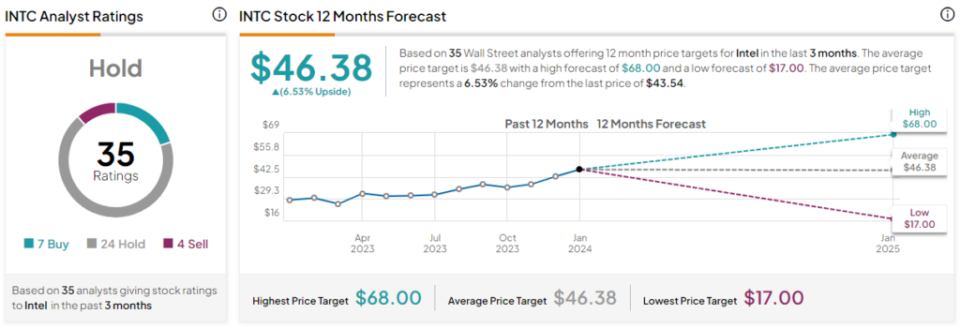

Is Intel Inventory a Purchase, In keeping with Analysts?

On TipRanks, INTC is available in as a Maintain primarily based on seven Buys, 24 Holds, and 4 Promote scores assigned by analysts previously three months. The common Intel inventory value goal is $46.38, implying 6.5% upside potential.

Conclusion: Ought to You Contemplate Intel Inventory?

Intel set the bar low for the present quarter. Buyers reacted badly to this, however that’s how alternatives come up. All of this might simply be a setup for an additional earnings beat and extra optimistic steering in just a few months.

It’s tough to check a very good end result when the market’s sentiment is so unfavourable about Intel. Keep in mind, although, that buyers favored Intel just some days in the past. They’ll come to understand Intel once more, I predict, so I really feel that it’s good to think about INTC inventory whereas it’s buying and selling at a decreased value.