As you could have discovered just lately, the “Magnificent Seven” is a gaggle of powerhouse shares together with Nvidia, Apple, and Microsoft, most of which have benefited considerably from the passion surrounding their synthetic intelligence (AI) efforts. However which might be the equal companies if the identical idea had been utilized to the healthcare sector fairly than the expertise sector?

Because it seems, there are solely 4 shares which have the suitable mixture of ongoing development and market-outperforming returns. All 4 of those magnificent healthcare corporations have stable enterprise fashions, upwardly trending share costs, and, sadly, considerably frothy valuations.

However additionally they have very lengthy development runways and a historical past of fine execution, so there is a stable likelihood that their worth tags might be justified by continued robust efficiency. Let’s meet the gamers.

Eli Lilly and Novo Nordisk

Eli Lilly (NYSE: LLY) and Novo Nordisk (NYSE: NVO) are two huge pharma shares that do not want a lot introduction because of the more and more absurd reputation of their smash-hit medicines for weight problems and sort 2 diabetes.

Eli Lilly makes the drug Mounjaro for diabetes in addition to Zepbound, which is identical remedy however formulated for weight reduction. It is the biggest healthcare firm by market capitalization with a dimension of $729 billion.

Novo Nordisk is the second-largest healthcare competitor by market cap, clocking in at $549 billion. It is accountable for the sort 2 diabetes drugs Ozempic, in addition to the obesity-oriented model of the identical drug, Wegovy.

Each corporations plan to proceed the method of penetrating those self same metabolic-disease markets, along with others, over the remainder of the last decade and past. Their pipelines are full of mid-stage and late-stage packages that would turn out to be the proper instruments in a smattering of various medical niches, or which might develop the indications and addressable market of their already-approved medicines.

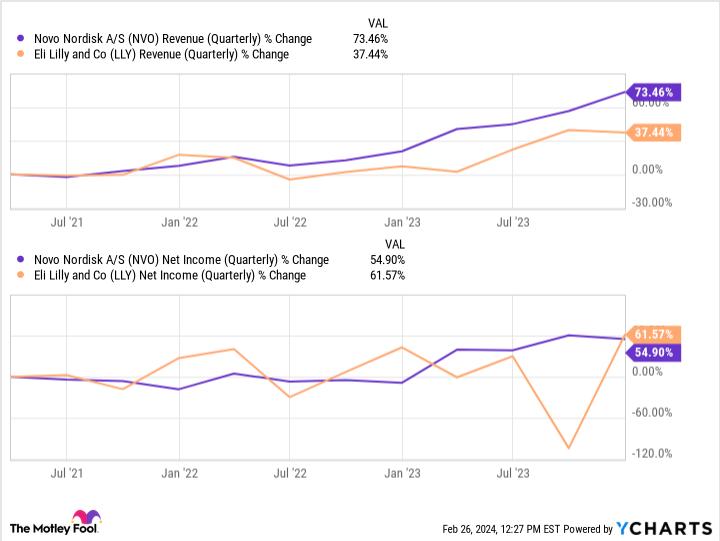

And neither firm anticipates a lot of an issue with competitors over market share, provided that the markets they’re excited about are tremendously deep and anticipated to continue to grow. Not satisfied that their trajectories are in step with magnificence? Take into account this chart under. As you’ll be able to see, they’re ramping up sharply, they usually’re value shopping for in case you do not thoughts their valuations.

Vertex Prescription drugs

Vertex Prescription drugs (NASDAQ: VRTX) is a drug developer specializing in uncommon illnesses like cystic fibrosis (CF). Lately, it commercialized a brand new gene remedy known as Casgevy for each sickle cell illness (SCD) and beta thalassemia with the assistance of CRISPR Therapeutics. Its market cap is $111 billion. And in fittingly magnificent style, its shares are up by a formidable 45% within the final 12 months.

One of many key issues that drives Vertex’s inventory to larger and larger heights is that its cystic fibrosis drugs, of which it is all the time producing and testing extra, are deeply entrenched available in the market. In reality, of the 92,000 identified sufferers with CF within the Western world, Vertex is presently treating all however 20,000 of those that are eligible.

On high of that, there isn’t any direct competitor for its gargantuan market share. And sufferers must take its medicines for all times to manage their signs.

With a secure base of income from gross sales of its CF medicine, the corporate has leeway to put money into analysis and growth (R&D) focused at bigger and extra aggressive markets, like for acute ache therapies. Which means it may well afford to take a whole lot of formidable photographs on aim with out overextending. And that is a giant a part of the explanation its trailing-12-month web earnings rose by 68% during the last 5 years, reaching $3.6 billion. As extra of its packages get permitted on the market, that determine will solely enhance, as will its share worth.

Intuitive Surgical

Final however not least is the robotic surgical procedure firm Intuitive Surgical (NASDAQ: ISRG), which boasts a market cap of $136.9 billion and a high line of $7.1 billion in 2023.

In its line of enterprise, prospects in hospitals first buy its da Vinci model robotic surgical models. Then they pay Intuitive for upkeep contracts, spare elements, new surgical toolheads, and coaching packages for surgeons, producing a protracted tail of recurring income over time.

The extra procedures prospects carry out with their da Vinci models, the extra recurring income it rakes in, and the extra the system turns into established as a workhorse in bariatric, urologic, and common surgical procedure working rooms.

And the competitors is, for now, nowhere to be seen. So it is no shock that Intuitive’s revenue margin, at 25%, is as vast as it’s. Contemplating that the demand for surgical procedure will not be going to say no anytime quickly, the shocking half is that the corporate is not already included within the present set of Magnificent Seven shares.

Do you have to make investments $1,000 in Eli Lilly proper now?

Before you purchase inventory in Eli Lilly, take into account this:

The Motley Idiot Inventory Advisor analyst staff simply recognized what they imagine are the 10 greatest shares for buyers to purchase now… and Eli Lilly wasn’t one among them. The ten shares that made the reduce might produce monster returns within the coming years.

Inventory Advisor offers buyers with an easy-to-follow blueprint for fulfillment, together with steerage on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than tripled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of February 26, 2024

Alex Carchidi has positions in Apple and Microsoft. The Motley Idiot has positions in and recommends Apple, CRISPR Therapeutics, Intuitive Surgical, Microsoft, Nvidia, and Vertex Prescription drugs. The Motley Idiot recommends Novo Nordisk and recommends the next choices: lengthy January 2026 $395 calls on Microsoft and quick January 2026 $405 calls on Microsoft. The Motley Idiot has a disclosure coverage.

These 4 Shares Are the “Magnificent Seven” of Healthcare was initially revealed by The Motley Idiot